The location playbook that governed data center site selection through 2022 relied on four primary criteria: land cost, fiber connectivity, proximity to enterprise customers, and state tax incentive programmes. Secondary considerations included power cost and reliability, climate for natural cooling advantage, and local construction labour availability. The playbook produced the concentration of data center capacity that exists today, massive clusters in Northern Virginia, Dallas-Fort Worth, Phoenix, and Northern California that grew because those markets offered competitive combinations of the primary criteria. That playbook is no longer adequate for selecting sites for AI data centers, and the operators and investors still applying it to current decisions are generating results that the market is already revealing to be systematically wrong.

Water rights and access have rapidly evolved from due diligence checkboxes to deal-breaking issues that require the same sophisticated analysis traditionally reserved for power procurement and real estate acquisition, according to Climate Solutions Legal Digest’s April 2026 analysis of data center transaction trends. Two-thirds of all data centers built or in development since 2022 are located in water-stressed areas like southern Arizona, the Colorado River Basin, and Texas, according to the World Resources Institute. The same markets that offered cheap land, available power, and favourable tax treatment through 2022 are now the markets where community opposition is most intense, water restrictions are tightest, and regulatory uncertainty is highest. The primary criteria of the old playbook were generating correct answers for the old era. They are generating systematically wrong answers for the current one.

Power Has Replaced Land Cost as the Dominant Location Variable

The transition from land cost to power access as the dominant data center location variable has been underway since 2023 but has accelerated to the point where it now determines site selection outcomes that all other criteria cannot override. A data center site with cheap land, competitive tax incentives, and strong fiber connectivity but no viable path to a grid connection on a commercially acceptable timeline is not a viable data center site, regardless of how attractive the other criteria appear. Grid connection queues averaging seven to ten years in primary US markets have created a situation where the first question in any serious site evaluation is not what the land costs but whether power is available and on what timeline.

Sean James, Nvidia’s distinguished engineer for energy systems, told Data Center World 2026 that power availability, not compute, is emerging as the limiting factor in AI data center development, and that behind-the-meter power is a good stopgap but not the preferred long-term solution. That framing reflects the current state of the market: operators are using on-site generation to bridge grid connection gaps, but the underlying constraint is a grid interconnection queue problem that behind-the-meter generation defers without resolving.

The sites commanding premium valuations in 2026 are those with firm grid connections already in place, power capacity that has already cleared permitting and interconnection processes, and utility relationships that provide visibility into future capacity expansion. Those assets are rare, and their scarcity is creating a power premium in data center site selection that the old playbook’s emphasis on land cost and tax incentives did not capture or value. Our long read on the time-to-power crisis as AI’s hidden scaling ceiling mapped the broader picture of why grid access has become the defining constraint in detail.

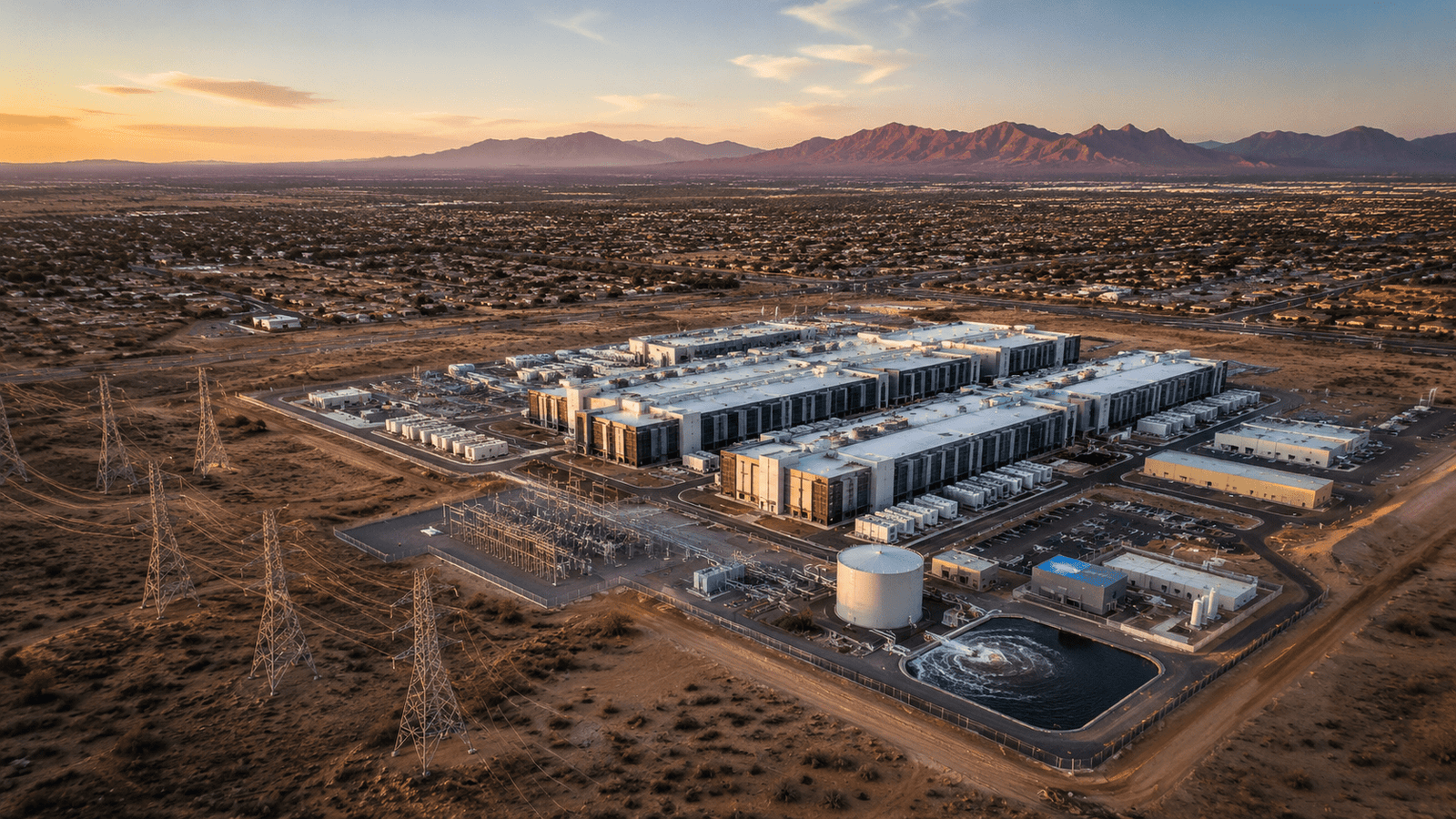

Water Has Become a Site Selection Variable With Permitting Implications

Water has moved from a secondary operational consideration to a primary site selection variable with permitting implications that can match or exceed electrical interconnection in timeline impact. Climate Solutions Legal Digest notes that water permitting timelines rival or exceed electrical interconnection queues, and that data center developers must now address water usage caps, tiered conservation triggers based on drought conditions, and community advisory mechanisms that were rarely seen in data center transactions five years ago. The water permitting complexity is not uniform across markets.

Western states operating under prior appropriation water law, where water rights remain separate from land rights and parties can litigate them independently of the development approval process, present a fundamentally different water risk profile from eastern states operating under riparian water rights frameworks. Consequently, developers applying western market site selection criteria to eastern markets must navigate a completely different legal and regulatory environment for water access.

The Cooling Technology Transition Is Changing Water Risk

The cooling technology transition from evaporative to liquid cooling is changing water consumption profiles in ways that affect both the magnitude and the regulatory treatment of data center water use. Evaporative cooling, which consumes water as it evaporates, is directly regulated by state and local water authorities and subject to drought-triggered curtailment in many markets. Liquid cooling systems that use closed-loop water circuits, recirculating the same water between chips and chillers rather than consuming it through evaporation, have materially different regulatory profiles because they withdraw water but return most of it. Microsoft estimates that its closed-loop water recycling systems at new Arizona and Wisconsin facilities starting in 2026 will each save approximately 125 million litres of water per year, reducing both the operational water footprint and the regulatory exposure that evaporative cooling creates in water-stressed markets.

Operators who design liquid cooling into their facilities from the ground up are not just making a technical infrastructure decision. They are making a site selection decision that determines which markets they can operate in without facing water-triggered regulatory risk. The water dimension of this shift is something our blog on water scarcity becoming AI infrastructure’s next binding constraint examined in depth.

Community Political Risk Has Emerged as an Independent Site Selection Variable

The community political risk dimension of data center site selection has emerged as an independent variable in the past 18 months that the old playbook did not include at all. Data Center Watch recorded that community opposition led to $98 billion in data center projects being blocked or delayed between March and June 2025. That figure represents a level of project risk from community opposition that no serious infrastructure underwriting model can treat as an acceptable tail risk. It is a standard operating risk that requires the same analytical rigour as power supply risk, water availability risk, and construction timeline risk.

The community political risk is not randomly distributed across markets. It concentrates in markets where the cumulative impact of data center development has become visible to residents through utility rate increases, water supply competition, and land use changes, and where organised opposition has had time to develop the infrastructure, legal expertise, and political relationships needed to successfully block or delay projects. Northern Virginia, Phoenix, and parts of Texas, the primary markets of the old playbook, now host the most developed community opposition ecosystems in the country. Our long read on the data center industry losing the public consent battle examined the structural nature of that opposition, and why it is not going away, at length.

Site selection models that quantify community political risk and incorporate it alongside power, water, and land variables are producing meaningfully different market rankings than models that treat community risk as a qualitative consideration. The operators who have built those models earliest are making location decisions in 2026 that will look prescient when the community risk dimension of the old playbook’s preferred markets becomes fully visible in 2027 and 2028.

The New Site Selection Hierarchy

The site selection hierarchy that emerges from these changed criteria looks materially different from the one that governed data center location decisions through 2022. Power access is now the primary criterion, evaluated on timeline to firm grid connection, available capacity, utility relationship quality, and behind-the-meter generation optionality. Water availability is the secondary criterion, evaluated on water rights position, regulatory framework, cooling technology compatibility, and community water stress levels. Community political risk is the third criterion, evaluated on opposition infrastructure maturity, utility rate impact visibility, cumulative data center impact, and local government posture toward new development. Land cost, tax incentives, and fiber connectivity still matter, but they now play a secondary role. They influence decisions within a constrained set of markets that already meet the primary criteria rather than determining which markets operators consider at all.

Which Markets Benefit From the New Criteria

This reordering changes which markets look attractive and which look overbuilt relative to their risk profiles. Markets that offer abundant renewable power with short interconnection timelines, water resources that support AI-scale cooling without community conflict, and limited existing data center concentration that has not yet generated organised opposition are the markets that the new site selection hierarchy favours. Several European markets, Norway, Spain, and parts of Poland, score better on this new hierarchy than they did on the old one. Several US markets, Northern Virginia, Phoenix, and parts of Silicon Valley, score worse.

The investment and development capital flowing into data center infrastructure is beginning to reflect this shift, though the pipeline of announced projects still reflects old playbook thinking that will generate the next generation of permitting challenges, community conflicts, and stranded development costs in markets that the new site selection criteria identify as high-risk. The permitting reform our article on what AI infrastructure permitting actually needs identified would help, but reform timelines will not close the site selection gap before the operators who adopted the new hierarchy earliest have already locked in their most defensible development positions.