The Shift No One Saw Coming

The global data center landscape has entered a phase where traditional metro hubs no longer dictate expansion patterns as they once did. Major cities that historically attracted hyperscale deployments now face constraints driven by land scarcity, escalating real estate costs, and limited grid flexibility. Demand for compute capacity has accelerated sharply due to enterprise digitization and the rapid scaling of artificial intelligence workloads, creating pressure that legacy hubs cannot absorb efficiently. Operators now confront prolonged permitting timelines, interconnection delays, and rising capital expenditure requirements that erode the economic viability of building in saturated markets. This shift reflects a structural imbalance between demand growth and infrastructure readiness rather than a temporary disruption in deployment cycles.

Capacity strain has become increasingly visible in leading data center clusters, where power availability dictates deployment timelines more than demand signals. Grid operators in these regions often struggle to approve large-scale connections due to transmission bottlenecks and competing industrial requirements. Developers now encounter multi-year delays for securing power, which directly impacts time-to-market for new facilities and undermines competitive positioning. The concentration of infrastructure in a few geographic pockets has also intensified systemic risk, prompting enterprises to reconsider geographic diversification strategies. Saturation has therefore evolved from a cost issue into a strategic constraint that shapes long-term planning decisions.

The economics of scale in traditional hubs have started to weaken as marginal costs rise disproportionately compared to emerging alternatives. Land acquisition alone can account for a significant portion of total project expenditure in metropolitan regions, often exceeding the cost of core infrastructure components. Operational expenses continue to increase due to higher energy tariffs and regulatory compliance requirements tied to urban environments. Investors and operators now evaluate opportunity cost more rigorously, factoring in delays and constraints that were previously overlooked. The resulting shift indicates that expansion decisions now prioritize feasibility over familiarity.

Market signals reveal that demand continues to surge, but supply constraints in core hubs prevent proportional capacity expansion. Hyperscale providers increasingly distribute workloads across multiple regions to mitigate concentration risks and improve resilience. Enterprise clients demand faster provisioning cycles, which legacy hubs cannot consistently deliver under current constraints. This divergence between demand growth and infrastructure readiness has created a structural incentive to explore alternative geographies. Consequently, the next phase of expansion is beginning to extend beyond historical patterns of clustering in major metros, with early signs of diversification emerging alongside continued concentration in established hubs.

When Power Moves, Compute Follows

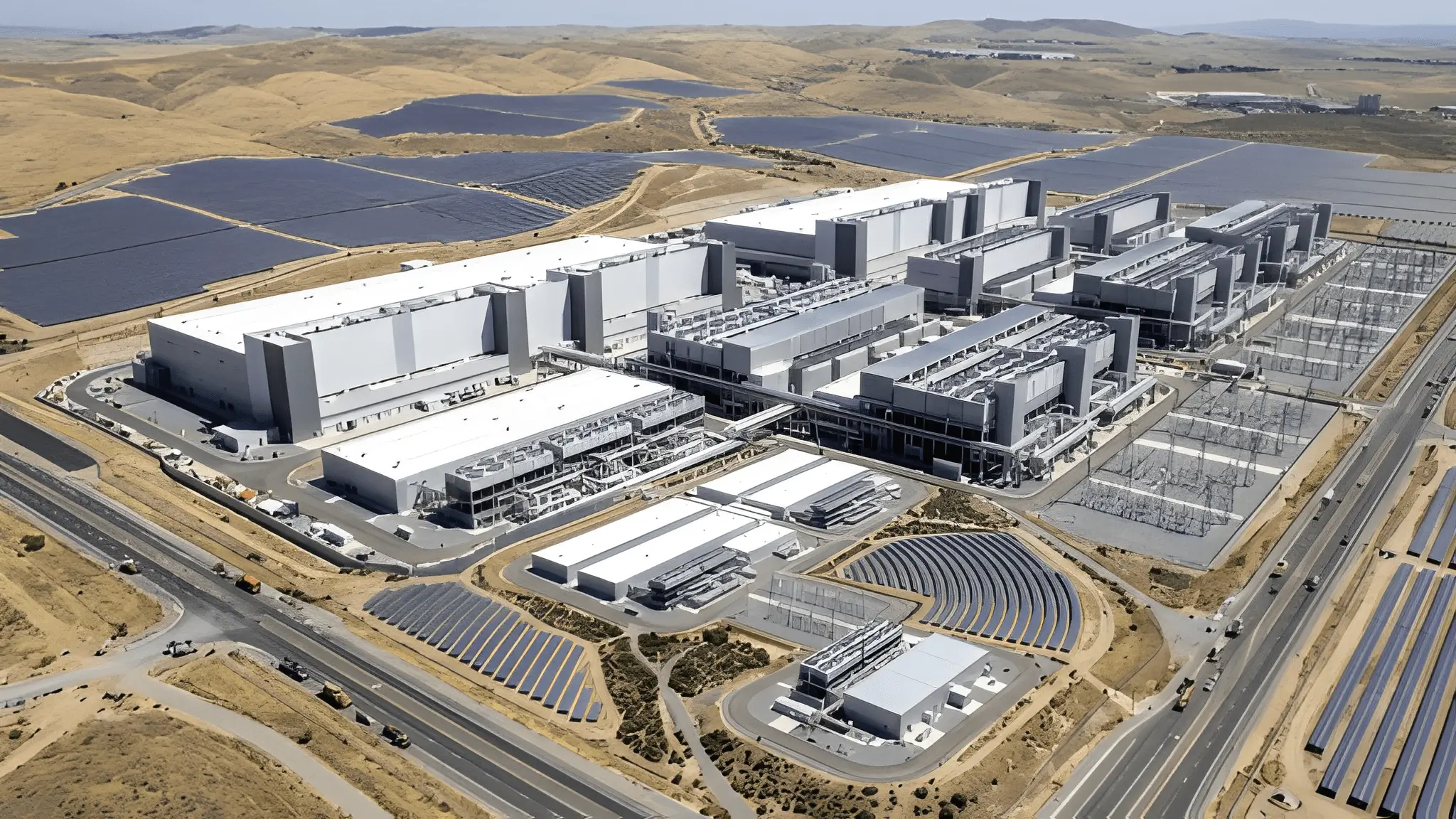

Energy availability has emerged as the primary determinant of where new data centers can realistically operate at scale. High-performance computing workloads, particularly those associated with artificial intelligence, require significantly higher power densities than traditional enterprise applications. This shift has transformed energy from a supporting input into a central strategic variable in site selection. Regions that can deliver reliable, scalable, and cost-efficient electricity now hold a decisive advantage in attracting large-scale deployments. The relationship between compute and energy has therefore become tightly coupled, reshaping geographic priorities.

AI-driven infrastructure introduces sustained energy demand that exceeds the design assumptions of many existing grids. Training large-scale models requires continuous high-load operations, which place stress on both generation and transmission systems. Operators now prioritize regions with surplus capacity or the ability to rapidly expand generation through renewable or conventional sources. Energy procurement strategies increasingly involve long-term agreements with utilities or direct investment in generation assets. This evolution underscores how energy infrastructure now drives compute deployment rather than merely supporting it.

In contrast to legacy hubs, emerging regions often provide access to underutilized energy resources that can support rapid scaling. Hydropower, wind, and solar capacity in these regions offer both cost advantages and sustainability alignment for operators seeking to meet environmental targets. Governments in such regions frequently incentivize large-scale energy consumption through favorable tariffs or policy support. Developers can secure power agreements more quickly, reducing project timelines and improving return on investment. This dynamic positions energy-rich regions as natural candidates for future expansion.

Power constraints in established markets have forced operators to rethink infrastructure deployment strategies at a fundamental level. Instead of optimizing for proximity alone, decision-makers now evaluate long-term energy security and scalability. This shift reflects a broader recognition that compute capacity cannot grow independently of energy infrastructure. Therefore, energy availability now acts as both an enabler and a limiting factor in global data center expansion.

The Rise of the ‘Unlikely’ Data Center Markets

Secondary cities and remote regions have begun to attract significant investment as operators search for viable alternatives to saturated hubs. These locations often offer abundant land, lower costs, and fewer regulatory barriers, making them attractive for large-scale development. Developers can design campuses with greater flexibility, incorporating modular expansion strategies that align with evolving demand. The absence of legacy constraints allows for more efficient infrastructure planning and execution. This shift reflects an emerging trend toward selective decentralization in digital infrastructure, although primary hubs continue to retain a significant share of global capacity.

Many of these emerging markets were previously overlooked due to perceived limitations in connectivity or ecosystem maturity. However, advancements in network technology have reduced the importance of proximity to traditional internet exchange points. Latency-sensitive workloads can still be supported through strategic network design and edge integration. Operators now balance performance requirements with the benefits of operating in less constrained environments. This recalibration has begun to elevate the strategic relevance of regions that were once considered peripheral, particularly for specific workload types and expansion strategies.

Land availability in these regions enables the development of large-scale campuses that would be impractical in dense urban environments. Operators can implement standardized designs across multiple facilities, improving efficiency and reducing deployment complexity. The ability to scale horizontally without significant land acquisition challenges provides a critical advantage in meeting long-term demand. This approach aligns with the needs of hyperscale providers that require consistent infrastructure across multiple locations. As a result, these regions are increasingly being evaluated alongside traditional hubs as viable investment targets for incremental and workload-specific capacity expansion.

Local governments in emerging markets actively compete to attract data center investments by offering incentives and streamlined regulatory processes. These initiatives often include tax benefits, infrastructure support, and expedited permitting procedures. Such policies reduce barriers to entry and accelerate project timelines, making these regions more competitive. The alignment between policy objectives and industry requirements further strengthens their appeal. Consequently, the rise of these markets reflects both economic and strategic alignment.

Infrastructure Is Following Opportunity, Not the Other Way Around

The traditional model of building data centers near established infrastructure has started to reverse as new regions gain prominence. Developers now initiate projects in locations that offer favorable conditions, prompting infrastructure providers to extend connectivity and support services. Fiber networks, for instance, increasingly expand into previously underserved areas to accommodate growing demand from data center operators. This shift suggests that in certain cases infrastructure development is beginning to respond more directly to emerging deployment opportunities rather than always preceding them. The dynamic represents a significant departure from historical deployment patterns.

Telecommunications providers recognize the long-term value of supporting data center growth in emerging regions. Investment in fiber connectivity and network capacity follows the initial establishment of compute infrastructure. This approach allows providers to capture new revenue streams while enabling broader ecosystem development. The interplay between data centers and connectivity infrastructure creates a reinforcing cycle of growth. As a result, regions that attract initial investment often experience accelerated infrastructure development.

Transport and logistics infrastructure also evolve in response to data center expansion in new geographies. Improved road networks and supply chain capabilities facilitate the movement of equipment and personnel required for large-scale projects. These developments contribute to the overall viability of emerging markets as long-term infrastructure hubs. The integration of multiple infrastructure layers enhances operational efficiency and reduces deployment risk. This progression highlights how opportunity drives broader economic development.

Investment patterns indicate that ecosystem development now follows anchor deployments rather than preceding them. Once a region establishes itself as a viable data center location, additional investments in supporting infrastructure tend to accelerate. This trend reinforces the attractiveness of these regions and encourages further expansion. The resulting feedback loop strengthens their position in the global data center landscape. Therefore, infrastructure growth is increasingly influenced by strategic deployment decisions, even though it remains a prerequisite in many established markets.

The New Trade-Off: Proximity vs Possibility

The evolving landscape introduces a fundamental trade-off between proximity to end users and the ability to scale infrastructure effectively. Traditional hubs offer low latency and established ecosystems, but they struggle to support long-term expansion due to constraints. Emerging regions provide scalability and cost advantages but may introduce latency challenges for certain applications. Operators must evaluate these factors based on workload requirements and business priorities. This trade-off shapes the architecture of modern data center networks.

Latency considerations remain critical for applications that require real-time interaction, such as financial trading or interactive services. However, many workloads, particularly those related to AI training and batch processing, tolerate higher latency levels. This distinction allows operators to distribute workloads across different regions based on performance requirements. The resulting hybrid approach balances proximity with scalability. It also reflects a more nuanced understanding of workload characteristics.

Cost considerations further complicate the decision-making process as operators seek to optimize both capital and operational expenditure. Emerging regions often provide lower costs for land and energy, enabling more efficient scaling. However, additional investment in connectivity and integration may offset some of these advantages. Decision-makers must therefore conduct comprehensive analyses to determine the optimal balance. This complexity underscores the strategic nature of location decisions in the current environment.

However, the trade-off between proximity and possibility does not represent a binary choice but rather a spectrum of options. Operators increasingly adopt distributed architectures that leverage multiple regions to meet diverse requirements. This approach enhances resilience and flexibility while optimizing resource utilization. It also aligns with broader trends toward decentralization in digital infrastructure. As a result, the industry continues to evolve toward more adaptive deployment strategies, combining both centralized and distributed models based on workload and regional constraints.

The Next Boom Will Look Nothing Like the Last

The next phase of data center expansion will diverge significantly from historical patterns defined by concentration in major metropolitan hubs. Growth will increasingly occur in regions that offer the necessary conditions for sustainable scaling, particularly in terms of energy and land availability. This shift reflects a broader transformation in how operators evaluate location decisions, prioritizing long-term viability over immediate proximity. The resulting landscape is expected to become more distributed and less predictable than previous cycles, while still maintaining strong concentration in a few dominant regions. Geography will therefore play a more strategic role in shaping outcomes.

The interplay between energy, infrastructure, and policy will determine which regions emerge as key players in the evolving ecosystem. Operators will continue to adapt their strategies to align with these factors, leveraging opportunities in emerging markets while managing risks. The industry will likely see increased collaboration between stakeholders to address challenges and unlock potential in new regions. This dynamic will drive innovation in both technology and deployment models. It will also redefine competitive dynamics across the sector.

Investment patterns suggest that the industry has begun to explore a more distributed model of growth, although expansion remains heavily anchored in established core markets. Early adopters that establish a presence in emerging regions may gain a competitive advantage as these markets mature. This trend underscores the importance of strategic foresight in navigating the evolving landscape. Operators must continuously reassess their assumptions and adapt to changing conditions. The ability to anticipate and respond to these shifts will define success in the next phase of expansion.

Ultimately, the transformation of the data center industry reflects broader changes in the global economy and technology landscape. The convergence of demand growth, energy constraints, and infrastructure evolution has created a new paradigm for expansion. Operators that recognize and adapt to these changes will be better positioned to capitalize on emerging opportunities. The next boom will not follow established patterns but will instead reflect a more complex and dynamic set of drivers. The industry now enters a phase where adaptability and strategic alignment determine long-term success.