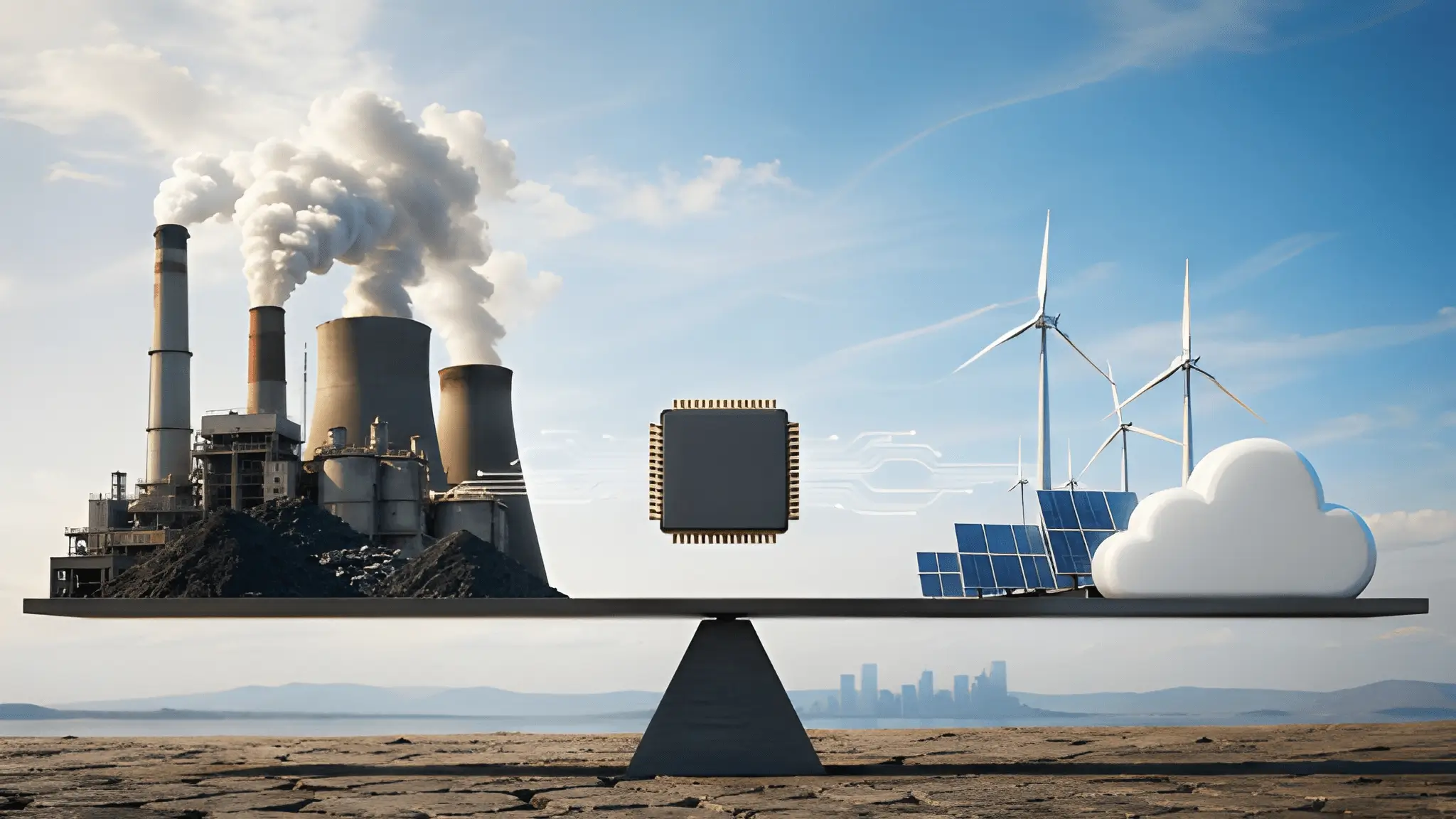

The global race to build digital infrastructure no longer depends only on technology roadmaps or capital availability. Energy systems are increasingly defining the pace, scale, and geographic distribution of infrastructure expansion across regions, alongside factors such as land availability, connectivity, and regulatory conditions. Markets that once relied on predictable grid evolution now operate under mixed signals shaped by political pressure, legacy dependencies, and shifting climate commitments. These contradictions do not stay theoretical because they directly influence site selection, deployment timelines, and operational risk for large-scale facilities. Industry leaders increasingly confront a landscape where ambition does not align with execution at the grid level. This misalignment introduces operational constraints that can slow progress and complicate long-term planning, particularly where energy system timelines diverge from infrastructure deployment cycles.

One Grid, Two Realities

Regions attempting to balance fossil continuity with clean transition strategies often create conflicting operational signals that ripple across infrastructure planning. In several regions, policymakers continue to approve short-term extensions for coal and gas assets while simultaneously announcing long-term renewable targets that often lack near-term execution clarity. Grid operators must therefore manage two parallel realities where legacy systems ensure stability while future systems remain under development. Infrastructure developers face difficulty aligning investment cycles with such dual-direction signals because planning horizons extend beyond policy timelines. Financial models increasingly account for uncertainty through risk adjustments as energy predictability shows variability across multiple jurisdictions. This divergence creates a fragmented planning environment that complicates both expansion and optimization strategies.

Energy contracts increasingly reflect this uncertainty as long-term agreements incorporate flexible clauses tied to regulatory shifts and grid reliability metrics. Hyperscale operators seek stable pricing structures but encounter volatility driven by policy reversals and delayed renewable integration. Regions that signal aggressive decarbonization without immediate grid readiness often struggle to meet the reliability thresholds required for large deployments. Meanwhile, legacy infrastructure continues to anchor supply, reinforcing dependence even as public commitments suggest otherwise. This tension creates inefficiencies that extend beyond pricing and into operational planning cycles. As a result, infrastructure decisions tend to favor regions with clearer execution pathways over those with ambitious but less defined implementation frameworks.

AI Demand Is Rising, Energy Direction Isn’t

The rapid expansion of artificial intelligence workloads has intensified demand for reliable, high-density energy supply across major markets. However, energy policy direction in many regions remains inconsistent, creating friction between infrastructure growth and grid readiness. Developers must navigate shifting regulatory frameworks that alter project feasibility even after initial approvals. Capacity planning becomes increasingly complex as future energy availability depends on policy outcomes rather than infrastructure readiness alone. This disconnect introduces delays that extend project timelines and increase overall deployment risk. Consequently, regions with unclear energy trajectories lose momentum despite strong demand signals.

Uncertainty around energy sourcing also affects supply chain coordination, particularly for high-density infrastructure clusters that require synchronized development. Equipment procurement, site preparation, and grid interconnection must align within tight timelines, yet policy ambiguity can disrupt deployment timelines and increase perceived risk for expansion, particularly in regions with evolving regulatory frameworks. In contrast, markets with inconsistent signals experience slower project execution despite available capital. This imbalance shifts competitive advantage toward regions that offer operational clarity rather than theoretical capacity. Ultimately, energy direction becomes a gating factor that shapes the pace of infrastructure expansion across global markets.

Legacy Power Is Quietly Shaping AI Futures

Legacy energy systems continue to influence where infrastructure clusters emerge, even as narratives focus on future technologies and sustainability goals. Regions with established coal or gas capacity often provide immediate reliability, making them attractive for large-scale deployments despite environmental concerns. Operators prioritize uptime and consistency, which legacy systems can deliver without the delays associated with new renewable projects. This dynamic creates a scenario where existing infrastructure can significantly influence the geography of modern digital ecosystems. Investment decisions often reflect current operational constraints rather than long-term aspirational targets, which can reinforce existing energy dependencies. As a result, infrastructure growth aligns more closely with current grid capabilities than future projections.

This influence extends beyond site selection into long-term strategic planning for infrastructure operators. Companies must evaluate whether regions can sustain future expansion while transitioning away from legacy systems. However, transition timelines often lack clarity, creating uncertainty about long-term viability. Operators often manage this risk by diversifying geographic presence, favoring regions with both existing capacity and more clearly defined transition plans. Meanwhile, regions that rely heavily on fossil extensions without clear transition frameworks face growing skepticism. This shift highlights how legacy systems continue to shape future outcomes even as policy narratives emphasize change.

The Approval Bottleneck No One Models

Regulatory approval processes increasingly act as hidden constraints on infrastructure expansion across multiple regions. Project timelines often extend beyond initial estimates due to layered approvals, environmental reviews, and political interventions. These delays create bottlenecks that disrupt synchronized development across energy and infrastructure projects. Developers must account for potential “call-ins” where higher authorities reassess approved projects, introducing additional uncertainty. This unpredictability affects not only timelines but also financial modeling and risk assessment frameworks. Consequently, approval processes become a critical variable that shapes deployment strategies.

Infrastructure planning models traditionally emphasize technical feasibility and capital allocation but often underestimate regulatory friction. However, recent project experiences indicate that approval delays can affect project viability even after substantial investment has been committed. Regions with complex regulatory environments experience slower infrastructure growth despite strong demand fundamentals. Developers are incorporating regulatory risk into site selection decisions, often favoring jurisdictions with more streamlined approval processes. This shift highlights the importance of governance efficiency as a competitive factor in infrastructure development. As regulatory complexity rises, approval bottlenecks become a defining constraint that few models fully capture.

Capital Doesn’t Wait for Policy Clarity

Investment flows in digital infrastructure increasingly respond to clarity rather than potential, reshaping global capital distribution. Investors and hyperscale operators allocate resources toward regions that provide stable policy signals and predictable energy frameworks. Markets that delay decisions or present conflicting signals risk losing capital to more decisive competitors. This reallocation occurs rapidly as capital seeks environments where deployment timelines align with strategic goals. Regions that delay decisions or present conflicting signals may face reduced investment flows compared to more policy-consistent competitors. Therefore, policy consistency emerges as a key determinant of competitive positioning in infrastructure development.

Capital mobility accelerates this trend as global investors compare regulatory environments across multiple jurisdictions. Regions that offer streamlined approvals and clear energy strategies attract sustained investment flows. In contrast, markets with higher uncertainty may experience reduced investment activity, which can limit their ability to scale infrastructure. This dynamic creates a feedback loop where clarity attracts investment, and investment reinforces growth. Over time, regions with consistent policies build momentum while others struggle to regain investor confidence. As a result, capital allocation increasingly reflects governance stability and policy clarity alongside resource availability.

You Can’t Run AI on Contradictions

Infrastructure growth now depends on alignment between energy systems and policy frameworks rather than isolated technological advancements. Regions that maintain contradictory signals between fossil reliance and clean transition commitments can create inefficiencies that may hinder infrastructure expansion. Stability in energy policy enables predictable planning, which remains essential for large-scale infrastructure deployment. Markets that prioritize clarity over ambition gain a competitive edge by reducing uncertainty across investment and operational decisions. This shift emphasizes execution over narrative, as stakeholders evaluate tangible outcomes rather than long-term promises. The evolving landscape reinforces the importance of coherence in shaping the future of global infrastructure systems.

Long-term success in infrastructure development requires consistent alignment between policy direction, energy availability, and regulatory execution. Regions that fail to achieve this alignment risk falling behind despite strong demand and available capital. Industry leaders increasingly focus on environments where stability supports sustained growth and operational efficiency. This approach reflects a broader shift toward risk-aware planning in a rapidly evolving global landscape. While ambition remains important, execution ultimately determines outcomes in infrastructure expansion. The path forward depends on resolving contradictions that currently define the global energy and infrastructure equation.