The SMR AI data center power narrative has been building for two years, and the announcements have come thick and fast. Google signed the world’s first corporate SMR purchase agreement with Kairos Power in October 2024. Microsoft revived Three Mile Island for 837 megawatts of carbon-free power. Meta partnered with Oklo to develop a 1.2 gigawatt nuclear campus in Ohio. Amazon secured 1.92 gigawatts through a long-term agreement with Talen Energy. The aggregate of these commitments represents a genuine strategic shift from the technology industry toward nuclear power as a solution to AI’s electricity problem.

It also represents a 2030 story that is being narrated as if it were happening in 2026. The first commercial SMR-powered data centers will not be operational until the end of this decade at the earliest. The regulatory timelines, the manufacturing challenges, the fuel supply constraints, and the first-of-a-kind construction complexity that apply to every nuclear project apply to SMRs as well. Investors evaluating nuclear energy’s role in AI infrastructure must account for the gap between announcement pace and delivery timelines when making infrastructure investment decisions today.

Why AI Created the Nuclear Moment

The interest in nuclear power from the technology industry is not irrational or driven purely by marketing. It reflects a genuine problem that renewables and grid power cannot fully solve on the timelines that AI infrastructure growth demands.

Solar and wind power are cheap, abundant, and scalable. They are also intermittent, generating power only when the sun is shining or the wind is blowing, and grid-scale battery storage capable of bridging multi-day periods of low renewable generation does not yet exist at the cost and scale required to make renewables a complete solution for 24/7 data center operations. Data centers need power all the time, at predictable levels, without the variability that renewable generation introduces. The capacity factor of solar and wind runs at 25 to 35 percent. Nuclear plants operate at capacity factors exceeding 90 percent, producing close to their rated output continuously.

The AI energy demand trajectory is forcing a nuclear rethink that goes beyond the incremental adjustments the power industry has been making for years. AI data centers will consume an estimated 945 terawatt-hours annually by 2030, equivalent to the entire electricity consumption of Japan. Goldman Sachs projects data center power demand will rise 160 percent by 2030. Meeting that demand with intermittent renewables requires either massive overbuilding of generation capacity, extensive long-duration storage that does not yet exist at commercial scale, or firm power sources that generate continuously regardless of weather conditions. Nuclear is the only zero-carbon firm power source that can be deployed at the scale these projections require.

Why Energy Cost Control Is the Real Driver

The competitive pressure dimension matters too. An AI infrastructure operator whose energy costs are lower because it has secured firm zero-carbon power at long-term contracted rates holds a structural cost advantage over competitors purchasing power on the spot market. Energy is the primary operational cost of an AI data center. The hyperscalers signing nuclear agreements are not just making sustainability commitments. They are making long-term energy cost management decisions that will compound into competitive advantages as AI infrastructure scales over the next decade.

What the Grid Cannot Provide

The time-to-power crisis is already the primary constraint on AI infrastructure expansion, and it interacts with the nuclear opportunity in a specific way. Grid connection delays in major US markets now stretch three to five years. The grid interconnection queue includes projects representing hundreds of gigawatts of capacity, but developers delay or abandon them when transmission and substation infrastructure does not come online in time.

Nuclear power, particularly SMRs designed for on-site or campus-adjacent deployment, offers the possibility of bypassing the grid interconnection queue entirely. An AI data center campus with its own dedicated nuclear power generation does not need a grid connection at the scale that a conventionally powered campus requires. It connects to the grid for backup and export purposes but generates its own baseload power independently. In markets with multi-year grid connection delays, grid bypass capability determines whether operators deliver a facility by 2027 or push delivery to 2030 regardless of construction start dates.

Why Scale Makes Nuclear the Only Viable Answer

The reliability argument compounds the availability argument. Grid power experiences interruptions, voltage fluctuations, and frequency deviations that data center operators manage through redundant UPS systems, backup generators, and power conditioning. On-site nuclear generation eliminates the dependency on external grid reliability and the associated capital cost of backup systems. A campus with dedicated nuclear generation and a grid tie for emergency backup is operationally more resilient than one that depends entirely on utility grid power.

The scale argument closes the case for why hyperscalers are willing to make long-term commitments to unproven technology. Each major hyperscaler is planning AI infrastructure deployments that will require gigawatts of firm power over the next decade. No other zero-carbon firm power technology can deliver gigawatt-scale baseload in the geographic flexibility that SMRs offer. Geothermal is limited to specific geological formations. Large hydropower requires specific river systems. Nuclear can be sited wherever regulatory approval and cooling water are available.

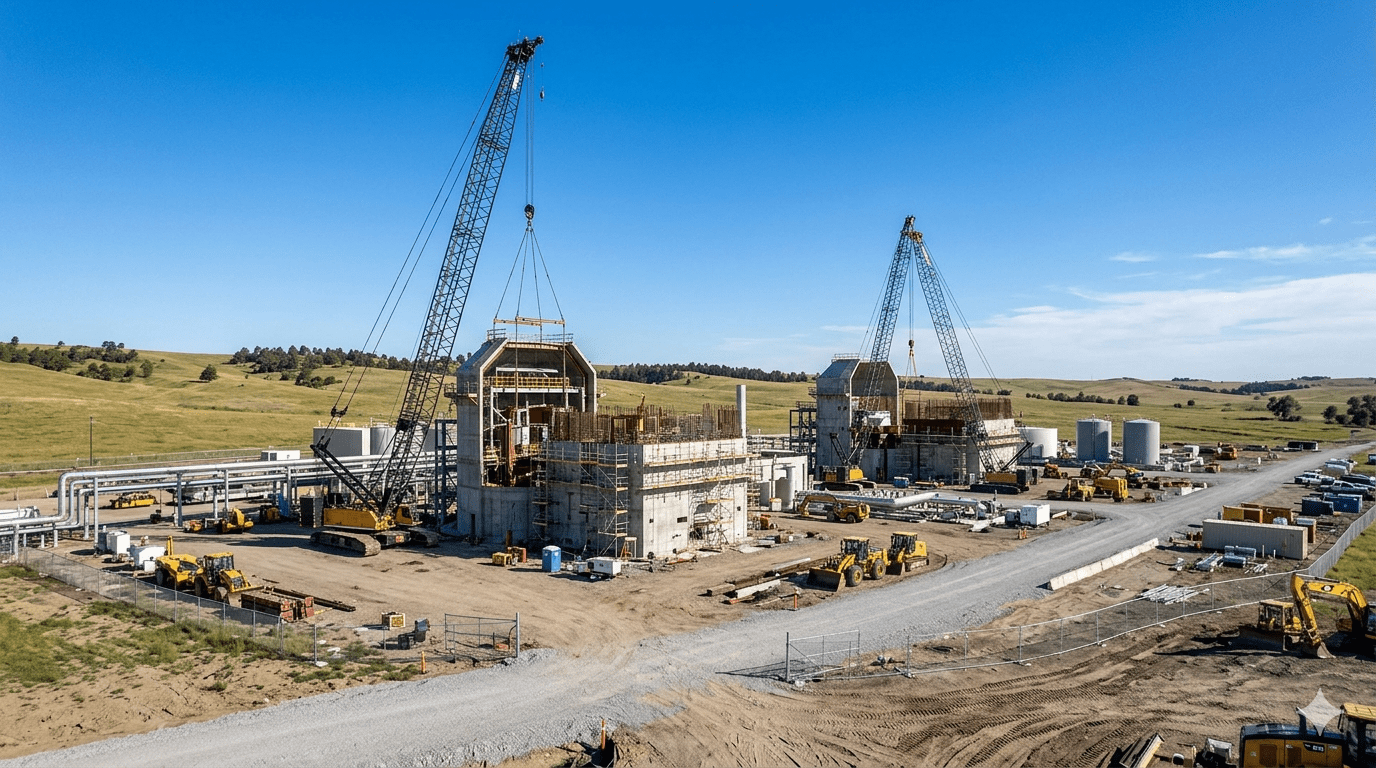

The SMR Landscape in 2026

Small modular reactors are not a single technology. They are a category spanning designs ranging from conventional light-water reactors scaled down to under 300 megawatts to advanced designs using molten salt, high-temperature gas, or sodium coolants that differ fundamentally from the light-water reactors that have powered commercial nuclear plants for decades.

The distinction matters for deployment timelines. Light-water SMR designs benefit from decades of regulatory experience and a well-understood safety case. NuScale’s VOYGR design was the first SMR design to receive design approval from the Nuclear Regulatory Commission. GE Hitachi’s BWRX-300, a 300-megawatt boiling water design, is in advanced licensing stages in multiple countries including Canada, the UK, and the US. These designs are closest to deployment because their regulatory pathways are clearest and their technology base is most familiar to regulators and construction teams.

Why Technology Diversity Creates Timeline Risk

Advanced reactor designs face a more complex regulatory journey. The NRC has no standardised approval process for molten salt or high-temperature gas reactors because the US has no operating experience with them at commercial scale. Kairos Power’s molten salt reactor uses fluoride salt coolant and a pebble bed fuel configuration requiring a novel safety analysis framework. TerraPower’s Natrium design uses sodium coolant with a molten salt thermal storage system. Both represent genuine engineering advances that require regulatory processes for which there is no established precedent.

The technology diversity in the SMR landscape reflects genuine uncertainty about which designs will prove most cost-effective at commercial scale. Factory manufacturing economics, which are central to the SMR value proposition, depend on design standardisation that requires volume production. The first few units of any SMR design will not benefit from factory learning economies. The fifth, tenth, and fiftieth units will, but only if the design achieves sufficient commercial traction to reach those production volumes. That selection process has not yet occurred in the SMR market.

The Deals That Have Been Signed

The hyperscaler nuclear commitments as of April 2026 represent a combination of existing plant power purchase agreements, SMR pre-purchase agreements, and direct investment in reactor developers. The distinction between these categories matters significantly for delivery timelines.

Microsoft’s Three Mile Island agreement with Constellation Energy is the most straightforward commitment. The agreement secures 837 megawatts over 20 years from an existing nuclear plant that operators built, ran, shut down in 2019, and are now restarting, with the project targeting first power in 2028 and offering the clearest delivery path among major hyperscaler nuclear commitments. Amazon’s agreement with Talen Energy for 1.92 gigawatts from the Susquehanna nuclear plant in Pennsylvania follows a similar model. These existing plant deals represent genuine firm power commitments on near-term timelines.

Google’s agreement with Kairos Power for 500 megawatts from six to seven molten salt reactors targets full deployment by 2035, with the first unit by 2030. Meta’s partnership with Oklo for a 1.2 gigawatt campus in Ohio has a Phase 1 target of 150 megawatts with first reactors expected operational by 2030. These are not power purchase agreements for operating capacity. They are agreements to purchase power if and when reactors that do not yet exist are built, licensed, and commissioned on timelines that no advanced reactor project has yet demonstrated it can meet.

The Bloom Energy comparison is instructive. Oracle signed a 2.8 gigawatt fuel cell agreement with Bloom Energy in April 2026. Bloom delivered a fully operational fuel cell system to Oracle in 55 days the previous year. The contrast between Bloom’s 55-day deployment and Oklo’s 2030 first-unit target captures precisely the gap between the firm power solutions available today and the firm zero-carbon power solutions that nuclear could deliver later this decade.

Why 2030 Is Optimistic, Not Conservative

The first-of-a-kind problem in nuclear construction stands as one of the most well-documented cost and schedule challenges in industrial history. Every first-of-a-kind nuclear build takes longer and costs more than the second because engineers identify unanticipated challenges only during construction. The AP1000 reactors built at Georgia’s Plant Vogtle came online years behind schedule and billions over budget despite being a proven light-water design with regulatory approval and an experienced developer.

SMRs are specifically designed to avoid this problem through factory manufacturing. The manufacturing model is theoretically sound. It is also largely unproven at commercial scale for any nuclear reactor design currently targeting the AI infrastructure market. The quality control processes, supply chain certifications, and manufacturing yields that determine whether factory-built nuclear components achieve their cost and schedule targets have not been demonstrated in practice for any of the designs with hyperscaler partnerships.

The manufacturing ecosystem for SMRs does not yet exist at the scale required to deliver the aggregate gigawatts that hyperscaler commitments imply. Precision component manufacturing for nuclear-grade components requires certified facilities, specialised materials testing, and quality assurance processes not present in conventional manufacturing infrastructure. Building that ecosystem takes years of investment before the first production units can be delivered. China’s Linglong One SMR, scheduled to begin commercial operations in the first half of 2026, will be the world’s first commercial onshore SMR if it achieves its timeline. Its performance will inform but not directly predict what American and European SMR projects will achieve given the different regulatory and industrial conditions.

The Regulatory Timeline Is the Real Constraint

Licensing a new nuclear reactor design in the United States is a multi-year process even for designs that build on existing regulatory experience. The NRC’s design certification process for a new SMR takes five to seven years from application to approval for light-water designs. Advanced reactor designs using novel coolants have no established regulatory pathway and are working through the NRC’s Part 53 rulemaking process, which is itself still being developed.

The NRC opened its Reactor Pilot Program in 2026 targeting first criticality for test reactors by mid-year at the Idaho National Laboratory. A test reactor achieving criticality at a national laboratory is the beginning of the data collection process that feeds into a commercial licence application, not the end of it. The data generated by the pilot programme will inform the safety analysis that regulators require, but the regulatory review process itself takes years to complete after that data is available.

Oklo’s licensing history illustrates the regulatory risk specifically. The company had its licence application rejected by the NRC in January 2022 on the grounds of insufficient technical information, submitted a new application in October 2023, and is working through the NRC’s review process. Meta’s contracted Ohio campus, which depends on Oklo’s Aurora Powerhouse receiving a commercial operating licence, cannot have its first unit operational by 2030 unless that licence is approved well before then and construction proceeds without delay. Each of those conditions is possible. None is guaranteed.

The Fuel Supply Chain Problem

Nuclear reactors require nuclear fuel, and the fuel supply chain for advanced SMR designs introduces a constraint that has received less attention than the reactor development timelines. Most operating nuclear plants use low-enriched uranium fuel enriched to less than five percent U-235. Several advanced SMR designs, including those from TerraPower and X-energy, require high-assay low-enriched uranium, or HALEU, enriched to between five and 20 percent U-235.

HALEU enrichment capacity in the United States is essentially non-existent at commercial scale. Russia’s Tenex has historically been the primary commercial supplier of HALEU-grade material, but the geopolitical complications of relying on Russian fuel supply for strategically significant energy infrastructure in 2026 are self-evident. The DOE has been funding HALEU enrichment capacity development, and Centrus Energy completed the first domestic HALEU production demonstration in 2023. Current domestic production capacity is far below what commercial SMR deployment would require.

Why Light-Water Designs Have the Clearer Path

Building commercial HALEU enrichment capacity requires years of investment in specialised centrifuge equipment, nuclear material licences, and regulatory approvals. The timeline for HALEU supply chain development is a direct constraint on the deployment schedule for HALEU-dependent reactor designs, operating in parallel with the reactor development and regulatory timelines. A HALEU-dependent advanced SMR that receives regulatory approval but cannot access commercial quantities of fuel at acceptable cost cannot generate power regardless of its technical merits or the size of the hyperscaler contract it has secured.

Light-water SMR designs using conventional low-enriched uranium fuel do not face the HALEU constraint, which is one reason they have clearer near-term deployment paths. The most innovative designs that have attracted the highest-profile hyperscaler partnerships tend to be the advanced designs that offer the highest efficiency and flexibility but require either HALEU or other specialised fuel configurations. The fuel supply chain is not an insurmountable problem. It is a problem that requires years of capital investment and regulatory work to resolve, and that timeline runs in parallel with reactor development rather than completing before it begins.

How Hyperscalers Are Managing the Uncertainty

The hyperscalers signing SMR agreements understand the timeline uncertainty better than the headline coverage suggests. Their contracting structures reflect it. Pre-purchase agreements for SMR capacity typically include provisions for delayed delivery, and the financial exposure at the time of signing is limited to prepayments and reservation fees rather than the full contract value. The headline gigawatt figures represent contracted capacity targets, not committed capital deployed against delivered power.

That contracting structure is rational for both parties. The reactor developer receives financial validation that helps attract further investment, regulatory engagement, and supply chain development. The hyperscaler secures a position in what will be a constrained market for firm zero-carbon power in the 2030s, without betting its infrastructure programme on technology that has not yet demonstrated commercial delivery. The option value of being a committed customer when SMR capacity is scarce in 2030 is real, even if the probability of on-time delivery is uncertain.

The operational risk management dimension is equally important. A hyperscaler whose energy strategy includes a meaningful fraction of SMR power by 2035 needs to ensure its near-term infrastructure can operate on available power sources while the SMR pipeline matures. The same companies signing nuclear pre-purchase agreements are simultaneously signing natural gas PPAs, deploying fuel cells, and securing grid connections in markets where capacity is available. That portfolio approach reflects the realistic understanding that nuclear power is a long-term energy strategy component, not a near-term power availability solution.

What Fills the Gap Until 2030

Firm power versus flexible power is the defining divide in AI infrastructure energy strategy, and the gap between nuclear ambition and nuclear delivery is precisely the space that natural gas, fuel cells, and aggressive grid connection strategies are filling right now. The power that AI data centers will consume between 2026 and 2030 will come from sources that are available today, not from sources that will become available when the first commercial SMR fleet reaches operating status.

Natural gas remains the primary gap-filler. It is dispatchable, available on short deployment timelines relative to nuclear, and capable of serving 24/7 baseload requirements without the variability of renewable generation. The same AI data center operators with sustainability commitments to zero-carbon power by 2030 or 2035 are building natural gas generation capacity to serve their near-term power needs, accepting the carbon cost as a transitional expense against the longer-term nuclear and renewable target.

Why Fuel Cells Are the Bridge Technology

Fuel cell technology is demonstrating that it can serve as both a near-term gap-filler and a bridge technology. Oracle’s agreement with Bloom Energy, announced in April 2026, captures 2.8 gigawatts of fuel cell capacity that can be deployed in weeks rather than years. Bloom’s solid oxide fuel cells operate at high efficiency, can use multiple fuel types, and produce reliable on-site power without grid interconnection delays. They are not zero-carbon on natural gas, but they are dramatically faster to deploy than any nuclear option and provide the on-site generation independence that reduces grid dependency in constrained markets.

The honest accounting of the AI infrastructure energy transition recognises that the path to zero-carbon firm power runs through a decade of transitional natural gas and fuel cell generation bridging between today’s grid-dependent infrastructure and tomorrow’s nuclear-powered campuses. The hyperscalers signing nuclear agreements today are making the right long-term decisions. The infrastructure they are building right now to serve AI workloads through 2030 is powered by entirely different sources.

The Long Game Worth Playing

None of the complexity outlined above negates the fundamental logic of the hyperscaler nuclear commitments. The firm power problem is real, the carbon commitment pressure is real, and nuclear is one of the few technologies that can address both simultaneously at the scale that AI infrastructure requires over the next two decades.

The reason to be precise about timelines and execution challenges is not to discourage nuclear investment. It is to ensure that infrastructure planning is calibrated to realistic delivery expectations rather than optimistic headline dates. A data center operator who builds a facility in 2026 expecting SMR power by 2028 is not building for nuclear. They are building for whatever power source is available by 2028, which in most markets means grid power, natural gas, or renewables with battery backup.

The policy and investment environment for nuclear power in 2026 is more favourable than it has been at any point in the past 40 years. The combination of AI demand creating unprecedented electricity appetite, the climate pressure driving preference for zero-carbon generation, the grid constraint creating value for on-site power generation, and the capital availability from technology companies willing to make long-term firm commitments has created conditions for nuclear investment that were not present during the post-Chernobyl and post-Fukushima decades. State-level legislation in Texas, Indiana, Tennessee, and other states is creating pilot programmes, cost recovery mechanisms, and tax incentives. The US and UK recently signed a Technology Prosperity Deal to streamline regulation and accelerate joint development of advanced nuclear technologies.

The Technology Risk That Remains Unresolved

Hyperscaler investors cannot easily manage one dimension of the SMR deployment challenge: reactor designs may fail to perform as developers project. Developers working on advanced reactors with novel coolants, fuel configurations, and thermal management approaches are tackling engineering problems that engineers have not yet solved at commercial scale. Molten salt reactors offer advantages in passive safety, high-temperature heat output, and fuel flexibility, but they also introduce materials compatibility challenges, tritium management requirements, and thermal cycling effects that engineers must validate through real-world operation before deploying commercial fleets.

The conservative technology path, represented by light-water SMR designs like the BWRX-300, reduces technology risk by staying close to proven engineering but accepts lower performance advantages over existing large reactors. The aggressive technology path, represented by advanced designs attracting major hyperscaler partnerships, offers superior long-term economics but carries risks that operators resolve only through commercial operation. The hyperscalers that have contracted for advanced designs are implicitly accepting that technology risk as part of the long-term firm power option they are purchasing.

The SMR sector is entering its execution era after years of design and policy development. The commitments are real, the technology is credible, the market need is genuine, and the policy environment is more supportive than it has been in a generation. The delivery timeline is what it is: the end of this decade for first units, the 2030s for meaningful fleet scale, and the 2040s for the fraction of AI infrastructure power that nuclear can realistically serve at the volumes the current growth trajectory implies. That timeline is worth investing for. It is not the timeline of a solution to the power problem AI data centers face today.