The AI infrastructure buildout has a hardware problem that is not about chips. It is about the industrial equipment that sits between the power grid and the server rack. That equipment is, consequently, becoming one of the most consequential supply constraints in the entire AI buildout cycle.

Transformers, switchgear, uninterruptible power supply systems, busways, cooling distribution units, and the cables that connect all of them are not exotic technology. They are, rather, the unglamorous backbone of every data center ever built. The companies that make them have been doing so for decades. The AI infrastructure buildout demands them at a scale, a speed, and a power density that the industry was not built to supply. That mismatch is, consequently, the root of the constraint. Pricing is not the issue. Demand signal clarity is not the issue. This is a structural gap between what the industry can produce and what AI infrastructure requires, and it is, specifically, not closing fast.

The $65 billion figure is a projection for global data center electrical and mechanical equipment spending by 2029. It comes from Wood Mackenzie analysis, corroborated by separate estimates from IDC and Gartner. It is nearly triple what the market was generating five years ago. The companies supplying that equipment, Eaton, ABB, Schneider Electric, Siemens Energy, Vertiv, Legrand, and a long tail of specialist manufacturers, have not come close to tripling their production capacity. They have not come close. The gap between what the AI infrastructure buildout requires and what the supply chain can deliver is, in turn, the central equipment market problem of 2026.

This is not a problem that money alone can solve. It is a manufacturing capacity problem and a raw materials problem. It is a skilled labour problem and a logistics problem. All of these are arriving simultaneously in a market built for steady, predictable demand rather than a vertical demand spike. The GPU shortage got the headlines. The equipment shortage is, however, the constraint that is actually delaying the most projects.

What the Equipment Market Actually Covers

Understanding the scale of the problem requires understanding what the equipment market actually covers and why each category is constrained in a different way.

Transformers: The Longest Lead Times in the Stack

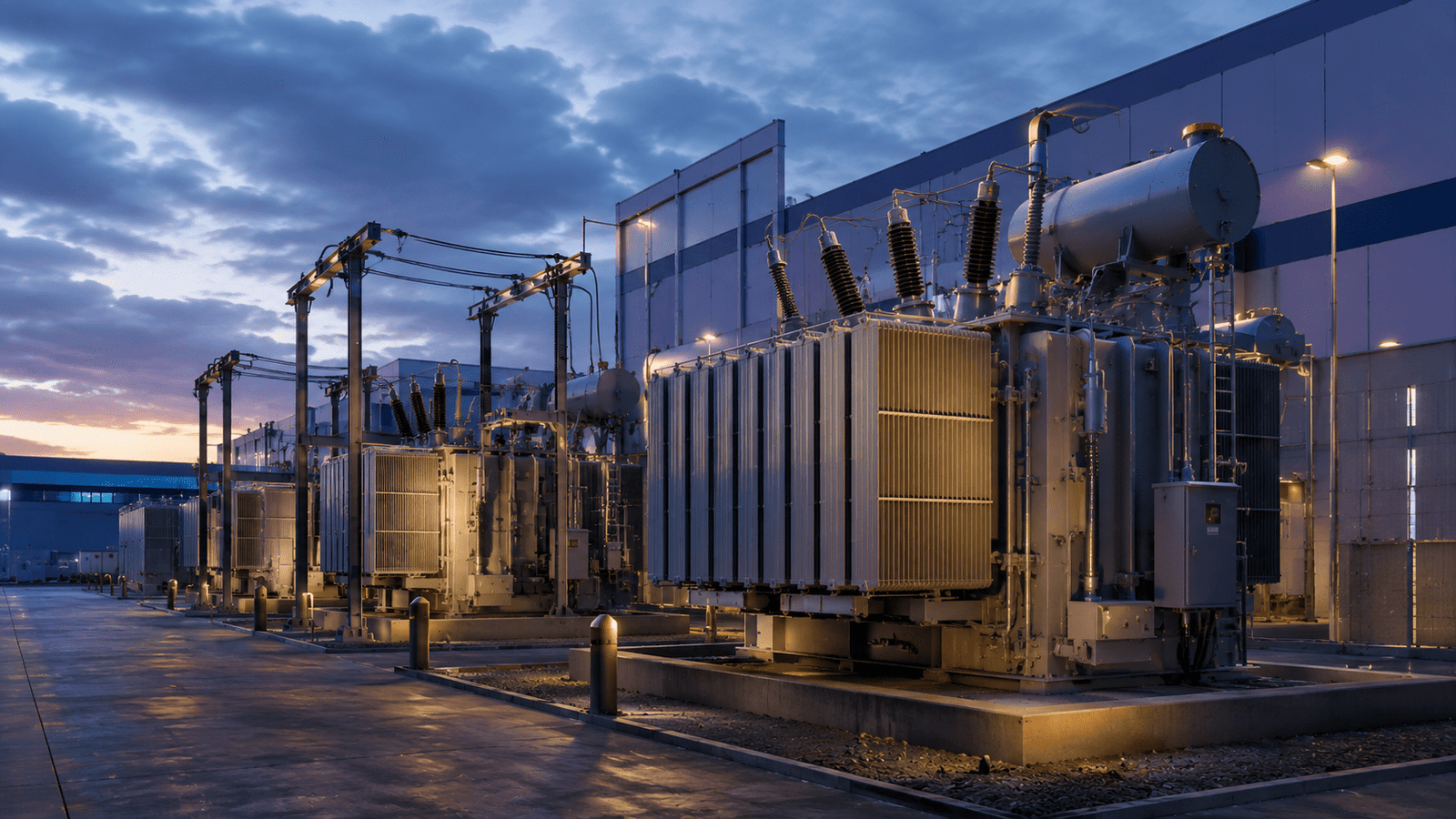

Transformers are the most acute constraint in the current equipment market. A large power transformer for a hyperscale data center campus is not a commodity product. It is a custom-engineered piece of equipment weighing hundreds of tonnes, built to order. It requires specialised steel, copper, insulating oil, and manufacturing expertise that exists in relatively few facilities worldwide. Lead times for large power transformers were twelve to eighteen months before the AI infrastructure boom. They are now running at two to four years for many specifications in primary AI infrastructure markets.

The transformer shortage has a specific structural cause that goes beyond simple demand growth. Transformer manufacturing is capital-intensive and requires highly skilled labour that takes years to train. The manufacturers who dominate the global market, ABB, Siemens Energy, Hitachi Energy, and a handful of others, have been operating near capacity for years. The AI infrastructure demand spike arrived on top of an already-constrained market. That market was also absorbing demand from renewable energy integration projects and grid modernisation programmes. Electrification initiatives across multiple industries were competing for the same supply simultaneously.

Tariffs have added a further complication. The tariff environment for electrical equipment from China has raised costs and complicated sourcing strategies for data center developers. China supplies a significant share of distribution-class transformers to the US market. That supply chain is, consequently, now more expensive and less predictable than it was. The piece our team published on why transformer lead times are now structurally reshaping AI infrastructure strategy covers this in detail Why Transformer Lead Times Are Now Structurally Reshaping AI Infrastructure Strategy is an Article in Power & Energy Grid that remains one of the most practically useful pieces we have published on this topic.

Switchgear and Power Distribution: The Hidden Queue

Switchgear is less discussed than transformers but faces similarly acute supply constraints. High-voltage switchgear for data center substations is, like large transformers, a custom-engineered product with long manufacturing lead times. Medium-voltage switchgear, busway systems, and power distribution units are somewhat more standardised. They are, however, also facing supply pressure that was not present before the AI infrastructure boom.

The switchgear constraint is, specifically, compounded by the shift to higher power densities in AI data centers. A rack that draws 30 kilowatts requires fundamentally different power distribution architecture than one drawing 120 kilowatts, which is increasingly standard for AI training infrastructure. Power distribution equipment built for legacy data center densities does not work for AI workloads. New equipment must be sourced. The manufacturers of that equipment are, in turn, working through order books that extend well beyond what most project timelines can accommodate.

The practical consequence is a hidden queue that does not appear in grid interconnection statistics but is equally capable of delaying a project. A data center campus can have its grid connection approved, its planning permission granted, and its hyperscaler customer contracted. It can still face a twelve-month delay because its substation switchgear is not available. That dynamic is, notably, playing out across multiple markets simultaneously in 2026.

Cooling Infrastructure: The Density Problem

Cooling equipment sits at the intersection of the equipment shortage and the AI density problem. Legacy air-cooled data center infrastructure targeted rack densities of 5 to 15 kilowatts. AI training clusters routinely require 100 kilowatts per rack or more. The shift from air cooling to liquid cooling requires equipment that is either not available at scale, not proven at the required power density, or both. Whether direct-to-chip, rear-door heat exchangers, or immersion, every liquid cooling approach faces supply constraints.

AI is, consequently, restructuring the cooling equipment market in ways that go beyond simple demand growth. The manufacturers of legacy precision air conditioning equipment are, in many cases, not the same companies best positioned to supply liquid cooling infrastructure at AI scale. New entrants, joint ventures, and product lines that did not exist three years ago are competing for this market. It is growing faster than any established manufacturer planned for. Supply chain constraints for cooling distribution units, manifolds, and the specialised fluids used in immersion systems are real. They are, in turn, adding to project delays across the AI infrastructure buildout.

Cables, Connectors, and the Last-Mile Problem

The cable and connectivity market is, in some respects, the least glamorous component of the equipment shortage and, consequently, the least covered. It is, however, a genuine constraint. High-voltage underground cable for data center substations has lead times that have stretched significantly as the AI infrastructure buildout has absorbed available manufacturing capacity. Specialised high-density copper busbars, fibre-optic cable for intra-campus connectivity, and the connectors and terminations that complete the system are all facing supply pressure. Pre-AI planning models did not account for any of it. That is not a criticism of the manufacturers or the developers who relied on those models. It is simply a description of a market that changed faster than any planning framework could track.

The Nvidia and Corning partnership to expand US optical connectivity manufacturing is a direct response to this constraint at the hyperscaler level. It is, specifically, an acknowledgement that the optical connectivity supply chain was not dimensioned for the bandwidth requirements of AI rack-scale architecture. That acknowledgement from the largest GPU vendor in the world is, notably, a signal. The supply chain constraint is being taken seriously at the highest levels of the AI infrastructure stack.

Why the Supply Chain Was Not Ready

The equipment market was not caught entirely off guard. Signals of accelerating data center demand were visible from 2022 onwards. Expanding manufacturing capacity for electrical equipment takes years, not months. The demand acceleration was faster than any planning scenario anticipated.

The Capacity Expansion Problem

Building a new transformer manufacturing facility requires land, environmental permits, specialised machinery, and a workforce trained in a craft that takes years to acquire. Total global manufacturing capacity for large power transformers does not, consequently, double in response to a demand signal, even a very loud one. The manufacturers who dominate the market have been adding capacity. They have been doing so, however, at the pace their own supply chains, labour markets, and capital structures allow. That pace is, in turn, significantly slower than AI infrastructure demand has grown.

Capital intensity in electrical equipment manufacturing also creates a specific reluctance to overinvest in capacity that might not be needed if AI infrastructure demand moderates. Manufacturers who over-expanded in previous demand cycles and faced utilisation problems when demand normalised are, understandably, cautious about repeating that experience. What results is a measured capacity expansion that is rational from each manufacturer’s perspective but collectively insufficient for the market.

The Raw Materials Constraint

Electrical equipment manufacturing is materials-intensive in ways that create supply constraints that go beyond factory capacity. Large power transformers require grain-oriented electrical steel, a specialist product manufactured in relatively few facilities worldwide. They also require significant quantities of copper, aluminium, and insulating oil. All of these materials face demand pressure not just from data center development. The electric vehicle market, renewable energy installation, and grid modernisation programmes across multiple continents are competing for the same supply simultaneously.

The grain-oriented electrical steel constraint is, specifically, the most acute raw materials bottleneck in the transformer supply chain. Global production of this material concentrates in a small number of facilities in Japan, South Korea, Germany, and China. Expanding production requires capital investment and lead times measured in years. The demand signal from AI infrastructure has, in turn, arrived at the same time as strong demand from wind turbine generators. Both require significant quantities of electrical steel. The competition for a constrained raw material across multiple high-growth end markets is, consequently, one of the deepest structural constraints in the equipment supply chain.

The Tariff Complication

The tariff environment has added a layer of complexity to equipment supply chains that was not present before 2025. Chinese manufacturers of electrical equipment supply a significant share of distribution-class transformers, switchgear, and power conversion equipment to global markets. They are now subject to tariff structures that have raised costs. In some cases those tariffs have effectively closed off sourcing options that data center developers had relied upon.

The tariff impact is not uniform across the equipment market. High-voltage transmission equipment has always come predominantly from non-Chinese manufacturers. Grid operators in primary markets require specifications that Chinese products have not typically met. Distribution-class equipment is, however, a different story. Chinese manufacturers have been competitive in this segment for years, and the tariff environment has disrupted supply chains that were working well. Our opinion piece examining this dynamic, The Tariff War on Chinese Electrical Equipment Is About to Slow Every Data Center in America, is an Opinion in Data Center that laid out the specific categories most exposed to tariff risk. The analysis there has, subsequently, been borne out by the project delay data that has emerged through 2025 and into 2026.

The Project-Level Impact

The equipment shortage is not an abstract market problem. It is manifesting in specific, measurable ways at the project level across the AI infrastructure buildout.

Schedule Slippage as the New Normal

The most visible project-level impact of the equipment shortage is schedule slippage. Data center projects planned on standard lead time assumptions are hitting delays because equipment is not available. The delays are, in some cases, measured in months. In others, the delays run to years. A project that cannot obtain its primary substation transformer on the right timeline has two options. Wait for the equipment, or redesign around a different power architecture. Neither option is fast or cheap.

The news we covered on electrical equipment shortages putting half of US data center projects at risk Electrical Equipment Shortages Put Half of U.S. Data Center Projects at Risk is a News piece in Data Center was initially treated as a supply chain story. It has, however, become a competitive strategy story. The developers who anticipated the equipment constraint placed orders early, in some cases before their projects had secured financing. They are, consequently, now holding delivery slots that their competitors cannot access. Equipment procurement has, consequently, become a form of optionality that sophisticated developers are treating as a competitive asset. The developers still treating equipment as a late-stage procurement task are, in turn, the ones accumulating the most schedule risk.

The Cost Inflation Problem

Equipment shortages drive price inflation in ways that compound project economics at exactly the moment when capital costs are already elevated. The cost of a large power transformer has increased significantly since 2022. Raw material inflation accounts for part of that. The pricing power that constrained manufacturers now hold in a demand-heavy market accounts for the rest. Switchgear, cooling infrastructure, and specialised cable have all seen similar price increases.

For data center developers operating on fixed-price contracts or tight return models, equipment cost inflation is a genuine financial problem. The projects that pencilled at 2022 equipment pricing are, in some cases, not pencilling at 2026 pricing. That dynamic is, in turn, contributing to project cancellations and deferrals that have shown up in data center construction pipeline data through 2025 and 2026. It sits alongside the more publicised demand moderation story around hyperscaler capex.

The Reshuffling of Developer Advantage

The equipment shortage is, notably, reshuffling competitive advantage across the data center developer market in ways that are not yet fully appreciated. The developers best positioned to manage the constraint are those with scale purchasing relationships, long-established supply chain partnerships, and the capital to place early orders. That profile maps most closely to the largest hyperscalers and the most established colocation operators. It does not map to smaller developers, new entrants, or the emerging class of AI-focused neoclouds that are trying to build infrastructure at speed.

The constraint is, consequently, functioning as a barrier to entry that reinforces the competitive position of established players. A hyperscaler that placed transformer orders in 2023 has a structural advantage over a neocloud that started planning in 2025. That advantage is not visible in any market analysis that focuses on GPU availability, power access, or financing. It is, however, real. It is, in turn, concentrating AI infrastructure buildout among a smaller number of well-resourced operators than the total pipeline of announced projects might suggest.

What Happens Next

The equipment market constraint is not permanent. Manufacturing capacity is expanding, supply chains are adapting, and the price signals from the current shortage are attracting investment in new production facilities. The question is whether those responses arrive fast enough to prevent the constraint from becoming a binding limit on AI infrastructure deployment through 2027 and 2028.

The Capacity Expansion Timeline

The major electrical equipment manufacturers have announced significant capacity expansion programmes in response to the demand signal from AI infrastructure and the broader electrification of the economy. ABB, Siemens Energy, Eaton, and Schneider Electric have all announced factory expansions and new production lines. Workforce expansion programmes are also underway. Together, these are, in turn, expected to add meaningful capacity over the next two to three years.

The timing, however, is the critical variable. A transformer factory expansion announced in 2025 and completed in 2027 does not solve the supply problem for projects that need equipment in 2026. Capacity expansion and AI infrastructure deployment timelines are, consequently, running in parallel rather than in synchrony. The gap between them is, specifically, the window during which the equipment constraint will be most acute. Projects that can navigate that window, through early ordering, design flexibility, or supplier relationships that give them priority access, will deliver on schedule. Those that cannot are already experiencing delays that are, in turn, reshaping the competitive landscape of AI infrastructure development.

Design Innovation as a Supply Chain Response

Some data center developers are responding to the equipment constraint not by waiting for supply to catch up but by redesigning their projects to reduce dependence on the most constrained equipment categories. Higher-voltage distribution architectures that reduce the number of transformation steps, and therefore the number of transformers required, are gaining traction in AI campus design. Modular power infrastructure that can be deployed incrementally, using available equipment rather than waiting for custom-specified units, is, similarly, attracting attention.

These design responses are, notably, not purely driven by the equipment shortage. Higher-voltage distribution improves efficiency and reduces losses. Modular deployment reduces upfront capital commitment and allows capacity to scale with demand. The equipment constraint has, however, accelerated adoption of approaches that might otherwise have taken longer to become standard practice. The supply chain problem is, in that sense, also functioning as an innovation accelerator for data center power architecture.

The Geographic Dimension

The equipment shortage is not uniform across geographies, which means it is creating a geographic dimension to AI infrastructure competitiveness that sits alongside the grid access and power availability dimensions. Markets where local manufacturing of electrical equipment exists have a structural advantage. Strong trade relationships with major equipment manufacturers provide the same benefit. Both are, specifically, advantages over markets that depend on long-haul supply chains for critical components.

The US has been investing in domestic electrical equipment manufacturing capacity through the Inflation Reduction Act and the CHIPS Act. Both include provisions for manufacturing infrastructure. Europe has its own industrial policy mechanisms driving investment in electrical equipment manufacturing. Markets in Asia with established electrical manufacturing bases have inherent supply chain advantages. Those advantages are, in turn, translating into project delivery advantages that are not yet fully reflected in competitive analyses of global AI infrastructure development. The Silent Bottleneck piece our team published is, specifically, worth reading alongside this analysis The Silent Bottleneck: Transformer and Substation Supply Chains is a Long Read in Power & Energy Grid that goes deeper on the geographic distribution of manufacturing capacity and its implications for global AI infrastructure deployment.

The $65 billion equipment market that AI is about to break is already breaking. Fractures are visible in project timelines, cost structures, and competitive dynamics across every major AI infrastructure market. Manufacturers who supply it are responding. They are responding, however, at the pace that complex industrial supply chains allow. That pace is, ultimately, not the pace that the AI infrastructure buildout demands. That gap is the defining supply chain story of AI infrastructure development in 2026, and it will remain so through at least 2028. The GPU shortage attracted the most attention because chips are visible and trackable. Equipment constraints are less visible. The equipment shortage is, in many cases, the more decisive one. It operates quietly, project by project, delay by delay. But its cumulative effect on the AI infrastructure buildout timeline is, consequently, significant and still growing.

The developers, operators, and investors who take the equipment constraint seriously will build faster and more reliably than those who do not. That means procurement timelines that reflect actual lead times rather than historical norms. It means investing in supplier relationships before they are needed. It means designing projects with supply chain flexibility built in from the start. The equipment market is, ultimately, not a problem that can simply be wished away or funded through. It is a physical constraint with a physical timeline. Understanding it precisely is, consequently, the first step toward navigating it effectively.

The Skilled Labour Gap Nobody Is Talking About

The equipment shortage has a human dimension that receives even less attention than the manufacturing capacity problem. Building, installing, commissioning, and maintaining the electrical infrastructure that AI data centers require demands skilled work. High-voltage electrical engineering, substation commissioning, transformer installation, and switchgear testing all require specialised expertise that takes years to develop. The global pool of engineers and technicians with these skills is, notably, not expanding at the pace that AI infrastructure demand requires.

The skilled labour gap manifests differently in different parts of the supply chain. At the manufacturing level, transformer and switchgear factories trying to expand production face a constraint on the skilled workers available to operate new production lines. At the project delivery level, data center developers face a constraint on the number of electrical engineers and commissioning specialists available to bring new facilities online. Both constraints are, in turn, real and both are, consequently, contributing to the timeline pressures that are affecting AI infrastructure projects across every major market.

The labour constraint is, specifically, harder to solve than the manufacturing capacity constraint. A new factory can, in principle, be built and equipped within two to three years. Experienced high-voltage electrical engineers, however, cannot be trained on any comparable timeline. A pipeline of engineering graduates entering the electrical power sector is, moreover, not growing at the rate the AI infrastructure buildout requires. In several major markets, the profession has faced recruitment challenges for years. The sudden surge in demand from AI infrastructure has, in turn, amplified those challenges without providing a mechanism to resolve them quickly.

The Secondary Equipment Market and Its Limits

One response to equipment shortages that has gained traction in the AI infrastructure market is the use of used and refurbished electrical equipment. Transformers, switchgear panels, and UPS systems from decommissioned facilities have always circulated in secondary markets. The AI boom has, notably, created unprecedented demand for equipment that would previously have gone to scrap or lower-specification applications.

The secondary market has genuine value as a short-term supply supplement. It is, specifically, most useful for developers with the engineering capacity to assess used equipment rigorously. Project flexibility to accommodate equipment that may need refurbishment before installation is also, in turn, required. A used transformer that meets the technical specification and arrives in weeks rather than years is, in practice, a viable option for developers facing timeline pressure. The secondary market has, however, real limitations. Used equipment carries unknown operational history and may not meet current specification requirements for AI-density installations. It is, in turn, available only as fast as legacy infrastructure gets decommissioned.

The secondary market is, consequently, a relief valve rather than a solution. It can absorb some of the pressure from the primary equipment shortage. It cannot, however, replace the primary market at the scale that AI infrastructure demand requires. Developers who rely heavily on secondary equipment are, also, making risk tradeoffs that may not be apparent until the equipment is in operation.

What Early Movers Did Right

The competitive divergence created by the equipment shortage is, already, visible in the market. The developers who recognised the constraint early and responded systematically are, consequently, in a materially better position than those who did not. Understanding what early movers did right provides a practical framework for how developers still facing supply chain challenges should be thinking.

The most important thing early movers did was treat equipment procurement as a parallel workstream rather than a sequential one. In conventional project development, equipment procurement follows financing, planning approval, and design completion. Early movers who recognised the supply constraint started procurement conversations with manufacturers before their projects had reached those milestones. They placed deposits, secured delivery slots, and in some cases committed to equipment specifications before their final designs were complete.

That approach carries its own risks. Equipment ordered speculatively may not match the final design requirements. Delivery slots secured early may not align with revised construction schedules. Early equipment deposits tie up capital that cannot go elsewhere. For developers with the financial flexibility to absorb those risks, early procurement has, however, proved one of the most effective strategies for managing timeline risk.

The second thing early movers did right was build direct relationships with manufacturers rather than relying solely on distributors and intermediaries. In a supply-constrained market, manufacturers allocate available capacity to their most established customer relationships. Developers who had invested in those relationships over years were, consequently, better positioned to secure priority access than those approaching manufacturers for the first time.