The AI infrastructure buildout has been narrated almost entirely as a capital story. Five hyperscalers committing $700 billion in 2026. Private equity funds deploying billions into data center construction. Sovereign wealth funds backing AI campus development across the Gulf, India, and Southeast Asia. The capital is real, the commitments are contractual, and the deployment velocity is genuinely unprecedented in technology infrastructure history. What the capital story systematically omits is a set of physical supply chain constraints that have no capital solution, because the constraint is not money. It is the lead time required to manufacture, ship, and install the electrical infrastructure that sits between a committed data center investment and an operational data center that can run a GPU.

Approximately 12 gigawatts of US data center capacity was expected to come online in 2026, according to Sightline Climate data cited by Bloomberg. Only approximately one-third of that capacity is currently under active construction. The remaining two-thirds, representing approximately 7 to 8 gigawatts of planned capacity, faces delays, schedule slippage, or outright cancellation, driven primarily by shortages of transformers, switchgear, and batteries. The primary cause is not insufficient capital. These facilities are funded. It is not insufficient demand. These facilities have committed customers. It is the availability of electrical infrastructure components whose manufacturing timelines are measured in years, not months, and whose production capacity cannot be increased through capital commitment on any near-term timeline.

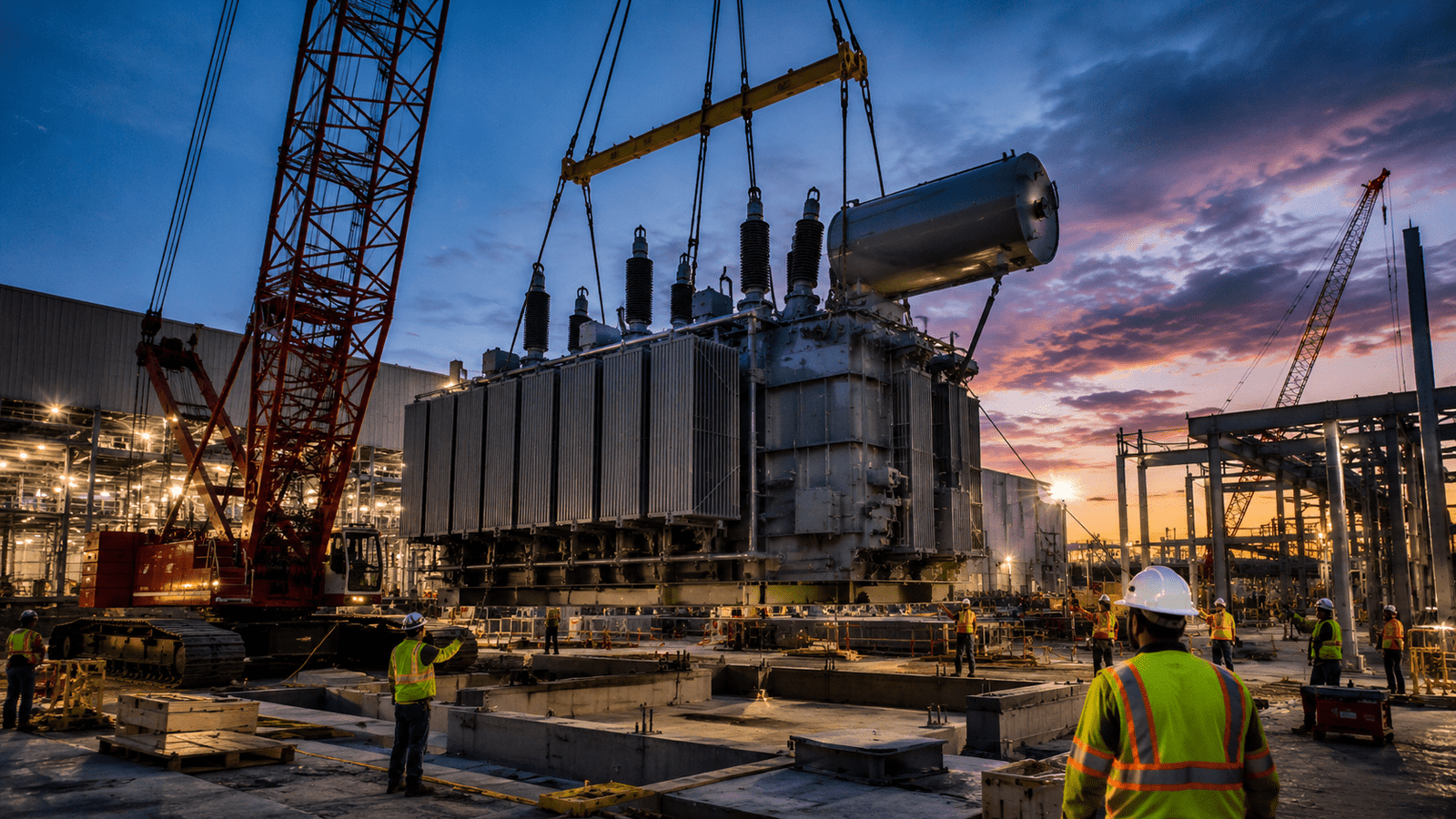

Electrical infrastructure represents less than 10% of total data center cost, but it is schedule-critical, because delays in any link of the power chain can halt an entire project. The industry spent three years worrying about GPU availability. The constraint that is actually stopping data centers from opening is a transformer.

The Transformer Bottleneck That Defines the Crisis

The transformer shortage is the most acute and least publicly discussed constraint in the AI infrastructure supply chain. Lead times for high-power transformers deteriorated sharply, typically 24 to 30 months before 2020, but now stretching to as long as five years, clashing with AI deployment cycles that can be under 18 months. High-voltage transformer prices have increased to nearly four times their 2021 levels, with lead times stretching from 16 weeks in 2021 to between 115 and 140 weeks in early 2026. A data center campus that secures land, financing, GPU allocation, and construction contracts in May 2026 but has not already placed its transformer orders cannot realistically expect to power on before 2028 at the earliest, and potentially not until 2030 in the markets with the longest interconnection queues.

The transformer shortage is structural rather than cyclical for reasons that extend beyond immediate demand. Transformers depend on grain-oriented electrical steel, a specialised material produced by only a handful of mills globally. That concentration creates fragility at the upstream level that cannot be resolved through conventional procurement diversification. Building new grain-oriented electrical steel production capacity requires multi-year capital investments in specialised industrial equipment that is itself subject to long lead times. The US does not currently have the domestic manufacturing capacity to produce high-power transformers at the scale the AI buildout requires, and expanding that capacity will take years regardless of the capital committed to the effort.

Procurement has become a core strategic competency in AI infrastructure development in a way that was entirely absent from how the industry thought about itself three years ago. Andrew Likens, energy and infrastructure lead at Crusoe Energy Systems, described the situation directly: if one piece of your supply chain is delayed, your whole project cannot deliver.

The Chinese Dependency That Compounds the Problem

The transformer shortage would be difficult enough to navigate if the US had robust domestic supply alternatives. It does not. US imports of transformers, switchgear, and lithium-ion batteries combined grew from $33.2 billion in 2020 to $77.1 billion in 2025, reflecting a structural dependency on imported electrical equipment that decades of domestic manufacturing decline have created. China is the world’s largest producer of electrical gear used to build and upgrade power infrastructure, both inside data centers and across the wider grid. The AI infrastructure buildout, which is the most significant expansion of US power-consuming industrial capacity in decades, is therefore dependent on supply chains from a country with which the US is engaged in an active trade conflict.

The tariff regime creates a specific and painful bind. Tariffs on Chinese electrical equipment add 15 to 25% to landed costs for components that are already on five-year lead times. An operator who pays the tariff premium to secure Chinese equipment still faces the lead time problem. An operator who refuses to pay the tariff premium and seeks non-Chinese alternatives faces even longer lead times from Canadian, Mexican, South Korean, or domestic suppliers whose production capacity for high-power transformers is more limited than China’s. On April 20, 2026, the White House issued a Presidential Determination under Section 303 of the Defense Production Act finding that grid infrastructure, including transformers and substations, qualifies as a national security priority, which enables certain emergency procurement authorities. That determination acknowledges the problem. It does not resolve the manufacturing capacity constraint that created it.

The Interconnection Queue Problem That Multiplies the Timeline

The transformer shortage operates within a broader grid interconnection challenge that compounds the timeline pressure from multiple directions simultaneously. Securing a firm grid connection for a new large industrial load requires navigating an interconnection queue that averages seven to ten years in primary US markets and can exceed fifteen years in congested markets like Northern Virginia. The interconnection queue delay predates the transformer shortage and is driven by different structural factors, primarily the volume of renewable energy projects competing for the same transmission infrastructure. But the two delays interact in a way that makes the combined timeline longer than either would produce independently.

A data center developer who secures a grid interconnection position and then faces a three-year transformer delay has a project that is delayed by the transformer, not by the grid. A developer who faces both a transformer shortage and an interconnection queue is navigating constraints whose resolution timelines do not overlap in ways that allow them to be parallelised. Grid connection processes require three to seven years, and critical equipment like transformers face multiyear lead times, creating a situation where industry analysis projects 30 to 50% of planned 2026 data center capacity will slip to 2028. The US interconnection queue has grown to over 2,100 gigawatts of pending requests, exceeding total installed grid capacity, meaning that every new large load addition joins a queue that is already longer than the entire US power system’s generating capacity.

Why Grid Interconnection Delays Make the Crisis Worse

The gap between announced AI infrastructure spend and operational AI infrastructure capacity is therefore not a temporary imbalance that will self-correct as capital flows in. It is a structural feature of a physical supply chain and grid interconnection system whose timelines are measured in years and whose capacity cannot be expanded by capital alone. The time-to-power crisis as AI’s hidden scaling ceiling documented the interconnection dimension of this constraint. The supply chain dimension has worsened significantly since that analysis was published.

The Domestic Manufacturing Response That Will Take Years

The US government’s response to the electrical equipment supply chain crisis has been to invoke emergency authorities and launch domestic manufacturing initiatives that are genuine policy responses but operate on timelines that do not address the immediate 2026 and 2027 delivery gap. The Presidential Determination under the Defense Production Act authorises the Department of Energy to accelerate domestic transformer manufacturing through priority rated contracts and financial assistance. The Inflation Reduction Act’s clean energy manufacturing provisions include incentives for domestic electrical equipment production. The CHIPS Act’s supply chain resilience provisions address semiconductor manufacturing but not the electrical infrastructure components that are actually on the critical path for data center delivery.

The fundamental challenge is that expanding domestic transformer manufacturing capacity requires building new industrial facilities, training specialist workforces, securing upstream material supply chains for grain-oriented electrical steel, and developing manufacturing processes that the US industry has not maintained at scale for decades. The fastest credible timeline for meaningful new domestic transformer production is three to five years from the point at which capital is committed to manufacturing expansion, which means the investment decisions being made now will produce manufacturing capacity that arrives in the 2029 to 2031 window.

The data center projects that need transformers in 2026 and 2027 will not benefit from domestic manufacturing expansion, regardless of how urgent and well-funded that expansion is. They will navigate the crisis through a combination of premium-priced imports, extended timelines, and the procurement strategies of the operators who were disciplined enough to place transformer orders three to five years ago when lead times were shorter and prices were lower.

The Battery Storage Dimension That Amplifies the Shortage

The transformer shortage does not operate in isolation. It is accompanied by a parallel shortage of battery energy storage systems and switchgear that amplifies its impact and creates additional critical path delays for data center projects that have addressed the transformer problem but face shortages in adjacent components. China supplies more than 40% of US battery imports, the energy storage component that provides backup power and grid services at every hyperscale campus. The tariff environment that makes Chinese transformer imports more expensive applies equally to Chinese battery systems, creating a situation where the two most strategically important components in the AI data center power stack are simultaneously more expensive and harder to procure than at any point in the market’s history.

The battery storage shortage has a specific impact on the behind-the-meter generation strategies that AI data center operators have developed as a response to grid interconnection delays. The logic of behind-the-meter generation is that an operator who generates their own power on-site can accept an interruptible grid connection rather than waiting for a firm connection, using battery storage to ensure continuous operation during grid curtailment events. That strategy reduces interconnection timeline from years to months in favourable markets. It depends on the availability of large-scale battery storage systems at commercially viable lead times and prices.

If battery storage is also on extended lead times at four times pre-surge prices, the behind-the-meter strategy that was supposed to circumvent the interconnection problem is itself subject to the supply chain constraints that make the interconnection problem so difficult to resolve. The solutions the industry developed for one constraint are running into the same supply chain bottlenecks as the constraints they were designed to solve.

The Switchgear Market That Nobody Talked About

Switchgear, the electrical equipment that controls, protects, and isolates electrical circuits within a data center’s power distribution system, is the supply chain constraint that has received the least public attention and is creating some of the most operationally damaging delays. A data center facility can have its transformer delivered and its grid connection secured and still face months of delay waiting for medium and high-voltage switchgear whose lead times have extended from four to eight weeks before 2020 to eighteen to thirty months in 2026. Switchgear is procured later in the construction timeline than transformers, which means the switchgear shortage has been less visible than the transformer shortage in early-stage project planning but is becoming the critical path constraint as more projects approach the commissioning phase.

The switchgear market shares several structural characteristics with the transformer market that make its shortage similarly difficult to resolve on near-term timelines. US domestic production capacity is limited. Import dependency on Asian manufacturers, including but not limited to Chinese suppliers, is significant. The technical specifications required for AI data center power densities at 100 kilowatts per rack and above require switchgear configurations that are not standard commodity products. The combination of extended lead times, non-standard specifications, and import dependency creates a procurement environment where the only reliable strategy is to order switchgear at the earliest possible stage of project development, before site selection is finalised and before construction timelines are committed to customer agreements.

The operators who treat switchgear procurement as a late-stage logistics activity rather than an early-stage strategic commitment are discovering that their commissioning timelines are controlled by equipment delivery schedules that have already been set by decisions made, or not made, twelve to eighteen months earlier.

The Geopolitical Dimension That Makes the Crisis Harder to Resolve

The supply chain crisis confronting AI infrastructure development has a geopolitical dimension that transforms it from a manageable procurement challenge into a structural policy problem that sits at the intersection of trade, national security, and industrial strategy. The US-China trade conflict has produced tariffs on exactly the categories of electrical equipment whose supply the AI buildout most urgently needs. The tariffs are intended to encourage domestic manufacturing, which is a legitimate long-term policy objective. Their near-term effect is to raise the cost and reduce the availability of equipment that the domestic manufacturing base cannot yet produce at the required scale, creating a transition period whose duration is measured in years and whose economic cost is borne by the same AI infrastructure investment that the policy is supposedly designed to support.

The national security concern runs in a different direction simultaneously. Grid infrastructure that is dependent on Chinese-manufactured components for its continued operation creates vulnerability to supply disruption, counterparty risk from export controls, and potential security concerns about hardware components from adversary-nation suppliers in critical infrastructure. The Presidential Determination under the Defense Production Act acknowledges these concerns. The practical response to them, however, requires building domestic manufacturing capacity that takes years to develop, creating a policy bind where the security concern argues for reduced Chinese dependency and the supply reality argues that immediate Chinese dependency cannot be eliminated without causing the very delays in AI infrastructure development that national security interests are supposed to prevent.

The Policy Tension Between AI Expansion and Supply Chain Security

The US government is simultaneously trying to accelerate AI infrastructure deployment for competitive and national security reasons, and trying to reduce the Chinese supply chain dependency that AI infrastructure deployment currently requires. Those two objectives are in direct tension, and the tension is being resolved in favour of neither clearly enough to give infrastructure developers the policy clarity they need to make optimal procurement decisions.

The Global Dimension Beyond the United States

The supply chain crisis affecting US AI infrastructure development is not a uniquely American phenomenon. The same transformer, switchgear, and battery shortages that are delaying US data center projects are creating parallel delays in European AI infrastructure development, Gulf sovereign AI infrastructure programmes, and the hyperscaler buildouts underway in India and Southeast Asia. The global nature of the constraint means that the alternative suppliers that US developers are turning to, Canadian, Mexican, South Korean, and European manufacturers, are receiving procurement enquiries from data center developers worldwide simultaneously. The result is that the alternative supply sources are themselves becoming capacity-constrained as demand from multiple markets converges on a manufacturing base that was sized for the pre-AI-buildout demand environment.

Denmark’s grid operator paused all new data center grid connection requests this week after total applications reached 60 gigawatts, three times the country’s total generation capacity. That pause reflects the same structural mismatch between AI infrastructure demand and physical delivery capacity that the transformer shortage reflects in the US. The mismatch is not primarily a transformer shortage in Denmark’s case, but the underlying dynamic is identical: AI infrastructure investment is arriving at a pace that the physical infrastructure systems governing its delivery cannot accommodate, and the resolution of that mismatch requires changes to physical systems that take years rather than months to implement. The US supply chain crisis is the most acute expression of a global phenomenon that will define the operational environment of AI infrastructure development through the end of the decade.

The Operators Securing Supply Chains Early Will Have the Advantage

The hyperscalers building vertical control over every layer of AI infrastructure documented, the operators who have secured their supply chains, power positions, and manufacturing relationships earliest are building competitive advantages that compound over time in a market where physical constraints govern delivery timelines regardless of financial resources. The supply chain crisis is not an obstacle that the AI infrastructure market will solve its way past. It is a structural feature of the physical economy that the AI infrastructure market will have to build around.

The Operators Who Solved the Problem Before It Was Visible

The supply chain crisis has created a two-tier market among AI infrastructure developers that is becoming more pronounced with every month of extended lead times. The operators who placed electrical equipment orders in 2021 and 2022, before the AI infrastructure surge created the current shortages, are bringing facilities online on schedule with equipment that was ordered at pre-surge prices and shorter lead times. The operators who entered the market in 2023, 2024, and 2025, attracted by the capital flows and announced demand of the hyperscaler buildout, are navigating the full severity of the current supply chain environment. The difference in delivery timeline and cost structure between these two cohorts is not marginal. It is the difference between projects that are profitable at current market rates and projects whose cost structures may not be supportable even at premium pricing.

The lesson that early movers demonstrate is one that the broader industry is now internalising under competitive and financial pressure: procurement leadership time is not a project management detail. It is a strategic competitive advantage that compounds across the AI infrastructure cycle in the same way that GPU allocation leadership compounded across the 2023 and 2024 cycle. Crusoe Energy Systems won the contract to build a major Texas data center campus partly by promising delivery speed, which it achieved through early orders securing electrical supplies before export barriers were erected.

The operators who are winning competitive positions in the current market are those who treated electrical equipment procurement with the same strategic urgency that the industry applied to GPU procurement eighteen months ago. The operators who treated procurement as a logistics function rather than a strategic one are the ones contributing to the 7-gigawatt gap between announced and deliverable 2026 capacity.

The Workforce Constraint That Nobody Is Counting

The supply chain crisis has a human dimension that the component shortage narrative consistently underweights. The electrical infrastructure that AI data centers require is not only constrained by the availability of manufactured components. It is constrained by the availability of the licensed electricians, power engineers, and specialist commissioning technicians needed to install and commission that infrastructure once it arrives. Goldman Sachs estimates approximately 760,000 additional power and grid workers will be needed by 2030, including 207,000 specialised transmission and distribution roles requiring three to four years of training. The training pipeline for those roles is not producing graduates at the rate the buildout requires, and the experienced specialists who can commission complex high-voltage infrastructure at AI data center specifications are in even shorter supply than the components they install.

The workforce constraint interacts with the component shortage in ways that multiply its impact. A project that secures its transformer delivery in month 18 still needs a qualified commissioning team available in month 18 to energise the facility on schedule. If every large AI data center project in a given market is reaching the commissioning phase simultaneously, the pool of qualified commissioning technicians who can work on those projects is distributed across a pipeline that is larger than the workforce can serve without queue delays that add weeks or months to project timelines beyond the component delivery delay.

Why the Workforce Bottleneck Could Become More Severe

The workforce bottleneck is less visible than the transformer shortage because it manifests as schedule variance rather than outright cancellation, but it is a real constraint that is extending commissioning timelines for facilities that have otherwise solved their component procurement challenges. The AI infrastructure buildout has an electrical engineering talent problem that is as structural as its transformer problem, and it is receiving a fraction of the policy and capital attention that the component shortage has generated.

What the Crisis Means for the AI Compute Market

The supply chain crisis has direct implications for the AI compute market that extend beyond the data center construction industry into the enterprise and neocloud operators who depend on new capacity coming online on the timelines their business models assume. The 7-gigawatt gap between announced and deliverable 2026 data center capacity represents AI compute that will not be available in 2026 despite being committed in financial models and hyperscaler guidance. Colocation vacancy rates in the Americas ended 2025 at approximately 4.2%, near historical lows. The new supply that would normally relieve that tightness is not arriving on schedule. Hyperscalers and AI developers who planned their compute capacity around announced 2026 delivery timelines are facing a gap between committed infrastructure spend and operational compute that additional capital commitment cannot close, because the bottleneck is physical components on five-year lead times, not money.

Why the Supply Chain Crisis Extends Beyond Data Centers

The implications for neocloud operators are particularly acute. A neocloud that signed a colocation agreement in 2025 expecting to take delivery of 50 megawatts of energised data center space in mid-2026 may find itself waiting until 2027 or 2028 if its colocation provider’s facility is among the approximately 7 gigawatts facing transformer-related delays. The financial model underlying that neocloud’s GPU financing assumes revenue from a 2026 go-live. A 2027 or 2028 go-live changes the debt service coverage ratio in ways that some operators will not survive without refinancing at less favourable terms. The supply chain crisis is therefore not just an operational problem for data center developers. It is a financial risk for the entire ecosystem of neocloud operators, GPU-backed debt structures, and enterprise AI deployment timelines that were modelled on announced infrastructure availability rather than actual delivery probability.

The Goldman Sachs chokepoint analysis that our article this week examined from an investment perspective is being confirmed in operational reality across the 2026 US data center delivery pipeline. The physical constraints are not theoretical. They are already determining which AI infrastructure commitments become operational capacity and which become extended timelines with deteriorating economics.

The Real Constraint Is Physical Delivery, Not Capital

The supply chain crisis is ultimately a story about the mismatch between the speed of financial commitment and the speed of physical delivery. Capital can be committed in days. Transformers take five years. The AI infrastructure market has been operating on the assumption that capital commitment is the binding constraint, which is why $700 billion in annual capex coexists with a 7-gigawatt gap between announced and deliverable 2026 capacity. Closing that gap requires not more capital but more time, more manufacturing capacity, more qualified workers, and more policy coherence around the supply chain dependencies that make the buildout simultaneously urgent and constrained. The industry that understands this clearly will plan and execute better than the one that continues to treat the supply chain crisis as a temporary disruption rather than the structural feature of the current AI infrastructure cycle that it actually is.

What Operators and Investors Must Do Differently

The supply chain crisis demands a set of operational and strategic responses from AI infrastructure operators and investors that differ fundamentally from the practices that worked when lead times were short and domestic manufacturing capacity was adequate. The most important response is treating procurement as a strategic function rather than an operational one, placing orders for transformers, switchgear, and battery storage at the earliest possible stage of project development rather than after site selection and customer commitments are finalised. The operators who are successfully navigating the current supply chain environment are those who have procurement teams that are as sophisticated and as senior as their real estate and capital markets teams, because the procurement decision is now as consequential as the financing decision in determining whether a project delivers on its committed timeline.

The Growing Gap Between Planning Assumptions and Delivery Reality

The second response is accepting that project timelines in the current environment require more conservative assumptions than the industry has historically applied. A project that assumes 18-month construction and commissioning timeline based on pre-surge lead times is a project that will disappoint its customers, its lenders, and its investors when the actual timeline extends to 36 months because of transformer and switchgear delays that were foreseeable at the time the project was underwritten. The financial models and customer agreements that are being signed today based on 2024 planning assumptions are building in schedule risk that will materialise in 2026 and 2027 delivery failures for the operators who have not updated their assumptions to reflect the current supply chain environment.

The gap between announcement-based planning and delivery-reality planning is where the next generation of AI infrastructure write-downs and customer relationship failures will originate. The operators and investors who close that gap earliest will navigate the supply chain crisis with the fewest casualties. Those who do not will discover that the physical economy does not adjust its lead times to accommodate financial model assumptions.