Europe has declared its AI ambitions clearly and repeatedly. The European Commission’s AI Continent Action Plan targets tripling EU data center processing capacity within five to seven years. The forthcoming Cloud and AI Development Act promises streamlined permitting and public funding for energy-efficient facilities. The EU has committed approximately €200 billion in AI and digital infrastructure investment through the decade. Every major policy document describes a continent mobilising to compete with the United States and China in the defining technology race of the era. The gap between what Europe says and what Europe can actually deliver has never been more visible than it is in 2026, and understanding that gap requires examining not the ambition but the physical, regulatory, and structural constraints that are preventing the ambition from materialising at the pace and scale the AI race demands.

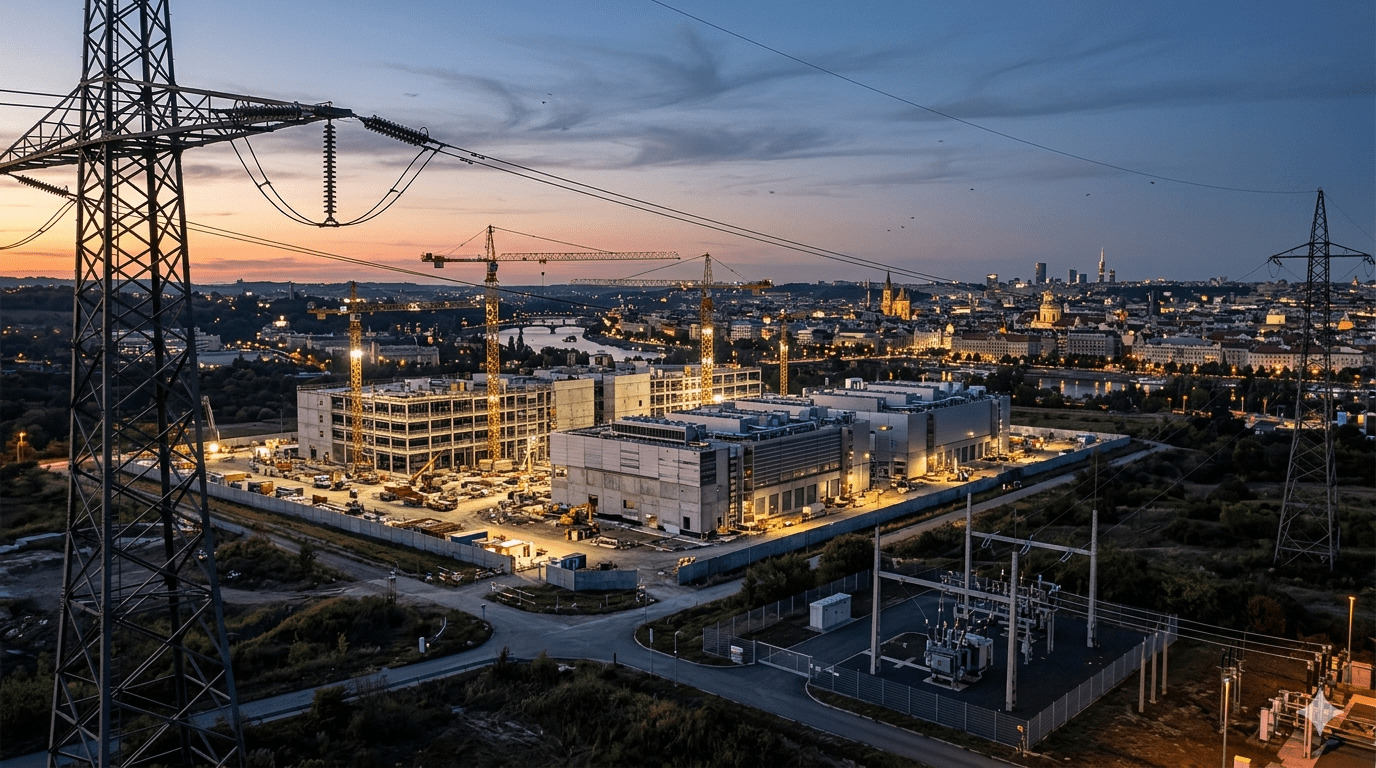

The United States currently operates roughly 5,400 data centers compared to approximately 3,400 across Europe, according to Cloudscene data. That gap is widening rather than narrowing, despite Europe’s stated policy commitment to closing it. The reason is not a shortage of capital, demand, or political will. Europe has all three. The reason is that the physical, regulatory, and energy infrastructure environment that AI data center development requires is systematically harder to navigate in Europe than in competing markets. Grid connection queues in the FLAP-D markets, Frankfurt, London, Amsterdam, Paris, and Dublin, now average seven to ten years. Permitting for large data center projects can take 18 to 24 months in the UK and longer in some continental markets.

Structural Constraints Are the Real Bottleneck

Germany now enforces waste heat reuse mandates that complicate site selection in urban markets. Dublin and Amsterdam have paused new data center connections as grid constraints continue with no clear near-term resolution. Europe is not losing the AI infrastructure race for lack of effort. It is losing because it has not yet built the structural foundations AI infrastructure requires, and because construction is not keeping pace with the urgency of global competition.

The Grid Constraint That Underlies Everything

The most fundamental constraint on European AI infrastructure development is the grid. Europe’s electricity transmission networks were not designed for the concentrated, high-density, continuous loads that AI data centers impose. The FLAP-D markets that host the majority of Europe’s installed data center capacity are precisely the markets where grid constraints are most severe, because those markets are already the most congested. Frankfurt, London, Amsterdam, Paris, and Dublin all face situations where new large-scale grid connections require major transmission infrastructure upgrades that can take a decade to plan, permit, and build. The European Union Agency for the Cooperation of Energy Regulators reported that direct grid congestion costs in the EU amounted to €4.3 billion in 2024 alone, before accounting for the indirect economic costs of project delays and investment deterrence.

The congestion problem is structural rather than temporary. Adding AI data center load at scale in markets where the grid is already congested does not simply require adding generation capacity. It requires reinforcing transmission infrastructure that often runs through urban environments where routing new lines or upgrading substations takes years of planning, environmental assessment, and public consultation. The IEA has described the fundamental timing mismatch at the core of the European grid challenge: a data center typically takes one to two years to build, while electricity infrastructure expansion requires much longer lead times.

In the European context, where regulatory and planning processes are more complex than in the US, those lead times for transmission infrastructure can approach or exceed the grid connection queue timelines themselves. A developer who secures a grid connection in a FLAP-D market after a seven-year wait may find that the transmission infrastructure needed to deliver the committed power is still under construction.

The Dublin and Amsterdam Lesson

The experiences of Dublin and Amsterdam represent the clearest case studies in what happens when AI data center demand exceeds grid capacity without adequate advance planning. Both markets paused new data center connections in 2022 and 2023 as their grid operators determined that available capacity could not accommodate additional large loads without destabilising the grid. Both have since partially lifted restrictions as new capacity has been commissioned, but neither has returned to the unconstrained development environment that characterised them in the mid-2010s when the foundations of their data center clusters were laid. The pauses themselves generated their own costs: projects in planning were delayed or abandoned, investment redirected to competing markets, and the pipeline of future capacity that would have been built in these markets without the pause now exists in other locations.

The Dublin pause is particularly instructive because Ireland is a small market where data center demand has become a disproportionately large share of total electricity consumption. Data centers now account for over 20% of Ireland’s total electricity use, a figure that makes data center demand a national energy policy question rather than a commercial infrastructure question. The Irish government’s response has been to introduce data center development restrictions that effectively limit new large-scale development in the Dublin market until grid capacity expansion catches up with existing demand. The result is that one of Europe’s most developed and strategically positioned data center markets is functionally closed to large-scale new development, redirecting investment to markets with less established ecosystems and less developed connectivity infrastructure.

The Regulatory Fragmentation That Amplifies the Problem

Europe’s regulatory environment for data center development is not uniformly restrictive. Individual markets within Europe offer genuinely competitive development environments. The problem is not that European regulation is universally hostile to data center development but that regulation is fragmented across member states in ways that create unpredictability, inconsistency, and compliance complexity that developers operating at scale find genuinely prohibitive.

A data center operator building a hyperscale campus in the US navigates federal permitting alongside state-level requirements. The regulatory framework, while complex, is ultimately unified under a national legal system with established processes and relatively predictable timelines. A data center operator building across multiple European markets navigates entirely different planning systems, grid connection processes, environmental assessment requirements, energy efficiency mandates, and data sovereignty frameworks in each jurisdiction. The compliance cost of this fragmentation is not merely additive. It compounds, because each market’s regulatory requirements interact with those of other markets in ways that create operational complexity across the portfolio that would not exist in a more unified regulatory environment.

Germany’s Waste Heat Mandate

Germany’s waste heat reuse requirement for new data center builds illustrates how individually reasonable regulations can create collectively problematic development conditions when deployed without adequate coordination with the infrastructure they assume. The requirement mandates that new data centers above a certain scale capture waste heat for productive reuse, typically through connection to district heating networks. The environmental logic is sound. Data centers generate substantial amounts of low-grade heat as a byproduct of their operations, and connecting that heat to district heating networks reduces the carbon footprint of both the data center and the buildings that would otherwise use fossil fuels for heating.

However, as JLL’s EMEA head of data center research Daniel Thorpe noted in the firm’s 2026 European market analysis, the municipal heat utilisation infrastructure that the waste heat requirement assumes is often not yet in place in the locations where data center development is commercially attractive. The regulation therefore steers data center development away from commercially optimal locations and toward locations with existing district heating networks, which tend to be in dense urban areas where other data center development constraints, including land cost, grid congestion, and planning complexity, are also most severe. The result is a regulation that pushes data center development toward precisely the markets where data center development is already most difficult, while simultaneously making it harder to develop in the markets where it would face fewer constraints.

The Permitting Pace Problem

The pace of permitting for large data center projects across Europe is incompatible with the speed at which AI infrastructure competition is moving. OpenAI’s statement explaining its decision to pause Stargate UK identified regulation as one of two primary barriers alongside energy cost. The company said it would move forward when conditions, including regulation, enable long-term infrastructure investment. That statement reflects a commercial assessment made by one of the most capitalised and motivated AI infrastructure developers in the world. If OpenAI cannot find the regulatory conditions it needs in the UK, the implication for smaller and less strategically positioned developers is clear.

Permitting timelines of 18 to 24 months for data center projects in some European markets compare unfavourably with what is achievable in competing markets in Southeast Asia, where some developments proceed from application to approval in a fraction of that time. The EU’s proposed Cloud and AI Development Act includes provisions for streamlined permitting, but legislation requires implementation, implementation requires member state action, and member state action takes time. The Centre for Future Generations, in its submission to the EU consultation on the Cloud and AI Development Act, notes that permitting processes in the EU often stretch beyond 48 months for strategic infrastructure projects. In a sector where progress is measured in weeks, that timeline is fundamentally incompatible with competitive AI infrastructure development.

The Markets Within Europe That Are Breaking Through

The picture across European AI infrastructure is not uniformly negative. Specific markets within Europe are succeeding in navigating the structural constraints that are limiting the overall European position, and those markets offer evidence of what the broader European environment needs to provide.

Spain is Europe’s fastest-growing major data center market by percentage growth, driven by a combination of factors that distinguish it from the constrained primary markets. The Spanish government has adopted hyperscaler-friendly policies that treat data center development as a national infrastructure priority rather than a commercial development requiring standard planning treatment. Spain’s role as a subsea cable landing point linking Europe to Africa and the Middle East gives it connectivity advantages that complement the policy environment. Additionally, the country’s renewable energy resource and the availability of land and water outside its major urban centres give it physical infrastructure advantages that overcrowded northern European markets cannot match. AWS and Microsoft have both committed significant investments to Spanish data center development, attracted by the same combination of factors.

Norway’s Renewable Advantage

Norway represents perhaps the most interesting European AI infrastructure success story precisely because it demonstrates that the constraints limiting the FLAP-D markets are not universal European constraints but specific consequences of the policy and infrastructure choices of particular markets. OpenAI’s Stargate Norway project is proceeding actively, powered entirely by hydroelectric energy, while Stargate UK is paused. The contrast between the two projects from the same developer illustrates the degree to which European AI infrastructure outcomes are determined by market-specific conditions rather than by any pan-European constraint.

Norway offers a combination of renewable energy abundance, cold climate for natural cooling, available land, and a regulatory environment that has been able to accommodate large data center development without the grid congestion and permitting complexity that characterise more densely developed European markets. As covered in our analysis of the time-to-power crisis as AI’s hidden scaling ceiling, the ability to access firm power on commercially viable timelines is the defining constraint of the current AI infrastructure buildout cycle. Norway offers that access in a way that London, Amsterdam, and Frankfurt currently cannot, and the investment flows reflect that reality.

The Policy Response and Its Limitations

The EU’s policy response to the AI infrastructure gap is substantive and reflects genuine recognition of the problem. The AI Continent Action Plan, the forthcoming Cloud and AI Development Act, the Data Centre Energy Efficiency Package, and the €200 billion AI and digital infrastructure commitment collectively represent the most ambitious European effort to close the AI infrastructure gap with the US and China. However, the policy response has three structural limitations that prevent it from closing the gap as quickly as the ambition implies.

The first limitation is the gap between Commission-level ambition and member state implementation capacity. The Commission can set targets, publish frameworks, and provide funding. It cannot override member state planning systems, accelerate grid infrastructure investment in specific markets, or compel local governments to approve data center developments that face community opposition. The tripling of EU data center capacity that the Cloud and AI Development Act targets requires member state governments to take actions at the planning and infrastructure level that the Commission cannot mandate. Progress will be uneven across member states and almost certainly slower in aggregate than the headline targets suggest.

The Sovereignty Tension

The second limitation is the tension between data sovereignty requirements and competitive infrastructure development. European data protection law, digital sovereignty policy, and AI regulatory frameworks collectively create compliance requirements for data center operators that competitors in the US and Southeast Asia do not face to the same degree. These requirements are not illegitimate. They reflect genuine European values around privacy, security, and technological autonomy. However, they impose compliance costs that reduce the attractiveness of European locations relative to alternatives, and they create regulatory uncertainty during implementation periods that makes long-term infrastructure commitments harder to justify.

The EU AI Act’s requirements for AI systems used in high-risk applications, the continued evolution of GDPR enforcement across member states, and the emerging requirements of the Cloud and AI Development Act all create a compliance environment that sophisticated operators can navigate but that adds cost, complexity, and timeline uncertainty to European data center development. Furthermore, the evolution of these frameworks is ongoing, which means that operators committing to long-term infrastructure investments are making those commitments in an environment of regulatory uncertainty that their US counterparts do not face to the same degree.

The Capital Mobilisation Challenge

The third limitation is the pace at which Europe mobilises capital for AI infrastructure compared with the United States and Asia. The €200 billion commitment is substantial in aggregate, but policymakers spread it across multiple programs, member states, and years, making it difficult to deploy at the concentrated scale and speed that AI infrastructure demands. A hyperscaler that commits $200 billion to data center construction in a single year can build infrastructure at a pace and scale that fragmented European public funding cannot match. European sovereign and institutional investors are engaging more actively in AI infrastructure, but European capital markets still rely on financing structures and timelines that do not match the capital intensity or speed required for competitive AI data center development.

The Competitive Markets Europe Is Losing Ground To

The markets that are capturing the AI infrastructure investment that Europe is failing to attract are not limited to the US. Southeast Asia, the Middle East, and select Asian markets are all absorbing investment that would have flowed to European locations in earlier technology cycles, driven by the same combination of faster permitting, more available power, and more predictable regulatory environments that Europe’s constrained primary markets cannot currently offer.

Singapore’s moratorium on new data center construction, imposed because its limited land and water resources cannot support further large-scale development, has accelerated development across the rest of Southeast Asia in ways that demonstrate how quickly investment redirects when constraints appear. Malaysia’s Johor state, immediately north of Singapore, attracted billions in new data center investment within months of Singapore’s moratorium as operators seeking Southeast Asian capacity shifted to an alternative that offered more headroom. The speed and scale of that redirection illustrates the competitive dynamics that Europe is navigating. When a constrained market imposes limits, capital does not wait for the constraints to resolve. It moves immediately to the next available alternative.

The Middle East’s Accelerating Position

The Gulf states continue to attract AI infrastructure investment at scale, despite the physical security risks exposed by the March 2026 drone strikes on AWS facilities in the UAE and Bahrain. They offer a combination of sovereign capital, political alignment, regulatory certainty, and power access that few regions can match. Saudi Arabia’s Humain program, the UAE’s national AI strategy, and Qatar’s computing infrastructure ambitions all draw on sovereign wealth and sustained political backing. This support creates a development environment in which the state addresses concerns around community opposition, permitting delays, and grid connection queues directly, rather than leaving them to commercial negotiation.

European democratic systems cannot replicate the Gulf’s model, but they still compete against the pace it enables. Investors and operators use that speed as a benchmark when making location decisions across both regions. India’s emergence as a major AI infrastructure market adds another dimension to the competitive landscape. Google’s $15 billion India AI hub, Microsoft’s $17.5 billion India commitment, and Amazon’s expanding Mumbai region all represent capital that is being deployed in India rather than in European markets where the same capital would face higher regulatory complexity and longer delivery timelines for equivalent or lower returns. The India AI infrastructure market offers a combination of domestic demand, government support, cost advantages, and improving power infrastructure that makes it an increasingly credible alternative to European locations for operators making regional capacity decisions.

The Workforce and Ecosystem Gap

The physical infrastructure constraints limiting European AI data center development are compounded by a workforce and ecosystem gap that receives less attention but carries equal weight for Europe’s competitive position. Building and operating hyperscale AI data centers requires specialists in high-density cooling, high-voltage power engineering, GPU cluster commissioning, and AI workload optimization. These skills remain in short supply globally and cluster in markets where the industry has developed over decades. Northern Virginia, Silicon Valley, Dallas, and Phoenix have built deep pools of experienced data center talent through sustained expansion. European markets, by contrast, draw from smaller talent pools that the current pace of development is already stretching.

The ecosystem of suppliers, contractors, and service providers that supports hyperscale data center development is similarly concentrated in primary US markets. Specialised construction contractors with experience in hyperscale data center builds, cooling equipment suppliers with installation teams trained for high-density liquid cooling, and commissioning specialists with experience in GPU cluster deployment are all more readily available in the US than in most European markets. Accessing these capabilities in European markets requires either importing them from the US, which adds cost and timeline, or developing them domestically, which takes years. Neither option is compatible with the development pace that competitive AI infrastructure requires.

The Digital Sovereignty Imperative

The one dimension of European AI infrastructure strategy that creates genuine long-term competitive advantage rather than additional constraint is the digital sovereignty imperative. European enterprises, governments, and regulated industries face data sovereignty requirements that mandate domestic processing of certain categories of sensitive data. That requirement creates a structural floor of European AI infrastructure demand that is not accessible to US or Asian providers operating from outside Europe, regardless of their cost or performance advantages. Healthcare records, financial data, government AI applications, and regulated industry workloads all represent categories where European data sovereignty requirements effectively require European infrastructure.

The digital sovereignty demand floor is growing as AI adoption accelerates across regulated European industries and as national governments implement AI applications in public services that require domestic processing. As covered in our analysis of the hyperscaler consolidation of AI infrastructure, the sovereign AI infrastructure segment represents one of the most defensible competitive positions available to European operators precisely because hyperscaler infrastructure cannot serve it regardless of its technical quality. Operators that build European AI infrastructure capable of meeting sovereignty requirements while securing competitive power access, permitting timelines, and operational costs will capture a demand segment that will grow alongside European AI adoption and remain structurally insulated from US and Asian competition. That is the opportunity Europe’s AI infrastructure strategy needs to centre on, rather than attempting to compete head-to-head with US hyperscalers on cost and scale across all workload categories.

The Financing Structures Europe Needs to Develop

The capital markets infrastructure that supports AI data center development in the US has no direct European equivalent, and that absence is a constraint that policy alone cannot address. US AI infrastructure financing has developed sophisticated instruments, including GPU-collateralized debt, sale-leaseback structures that separate real estate from compute assets, and publicly traded REITs that provide institutional investors with liquid exposure to data center real estate. These instruments allow US developers to access capital at lower cost and higher speed than the bank lending and private equity structures that dominate European infrastructure finance.

European capital markets for AI infrastructure are developing but lag their US counterparts by several years in both product sophistication and investor familiarity with the asset class. European institutional investors, including pension funds, insurance companies, and sovereign wealth vehicles, have substantial capital seeking infrastructure investment but have historically allocated most of it through structures that prioritise stability and predictability over the rapid scaling that AI infrastructure requires. The mismatch between the capital availability of European institutional investors and the deployment characteristics of AI infrastructure is a genuine financing gap that innovative structures could address.

The EIB’s Potential Role

The European Investment Bank has the scale, mandate, and political backing to play a catalytic role in European AI infrastructure financing that no private capital provider could play alone. The EIB has historically been a major financing partner for European infrastructure projects across energy, transport, and digital connectivity, and its participation in AI infrastructure financing could help establish the asset class credibility and standardise the financing structures that European private capital needs before it will deploy at scale. A dedicated EIB AI infrastructure facility, offering first-loss protection or subordinated debt to de-risk private capital deployment in European AI data center development, could mobilise private capital at multiples of the EIB’s direct commitment by reducing the risk premium that private investors currently require for a new and relatively untested asset class.

Several European member states are exploring analogous instruments at the national level. France’s sovereign AI fund, Germany’s KfW financing programs for digital infrastructure, and Nordic sovereign wealth participation in data center development all represent national-level efforts to bridge the gap between available private capital and the deployment characteristics of AI infrastructure. These efforts are moving in the right direction but are fragmented across member states in ways that limit their aggregate impact. Coordinating these national financing mechanisms through EU-level frameworks would increase their effectiveness without requiring the politically difficult centralisation of budget authority that pan-European fiscal instruments require. The capital is available in Europe. The structures that would deploy it effectively at AI infrastructure scale are still being developed.

What It Would Actually Take to Change the Outcome

The honest assessment of what it would take for Europe to close the AI infrastructure gap is uncomfortable because it requires acknowledging that the gap is not primarily a funding problem or a political will problem. It is a structural implementation problem that requires changes at the member state level that no Commission initiative can deliver by itself.

Closing the grid connection queue in FLAP-D markets requires building transmission infrastructure, a process that takes a decade. No policy announcement can shorten that physical timeline. Policy can, however, ensure that governments make the necessary decisions immediately, commit funding without tying it to future budget cycles, and sustain political will across elections and changes in government. Europe’s track record on long-term infrastructure investment at this scale remains mixed, and the AI infrastructure moment demands a level of consistency that European political systems have not always demonstrated.

The Permitting Reform Imperative

Closing the permitting gap requires member state governments to cut planning timelines for data center projects from years to months. Policymakers already have the tools to do this. The EU’s Renewable Energy Directive sets an 18-month permitting deadline for renewable projects in designated areas, showing that when governments act with intent, permitting systems can move quickly. Extending similar fast-track mechanisms to AI infrastructure would require each member state to make explicit political choices that balance economic development against planning system integrity and community consultation rights. Those choices are difficult. They force trade-offs between speed and legitimacy that democratic systems typically resolve slowly. The AI infrastructure race is not waiting for those deliberations to unfold at that pace.

The markets that break through these constraints — Spain, Norway, Poland, and Finland among them — are the ones that can demonstrate that European AI infrastructure ambition can be matched by European AI infrastructure delivery. They will attract the investment that builds the track record that attracts more investment. Meanwhile, the markets that cannot resolve their grid and permitting constraints will watch that investment flow elsewhere, not to competitors in the US or China, but to their European neighbours who figured out how to move faster. The Europe AI infrastructure race is not lost. It is being contested market by market, decision by decision, and grid connection by grid connection. The aggregate European position is losing ground. The question is whether enough individual markets can move fast enough to prevent that loss from becoming permanent.