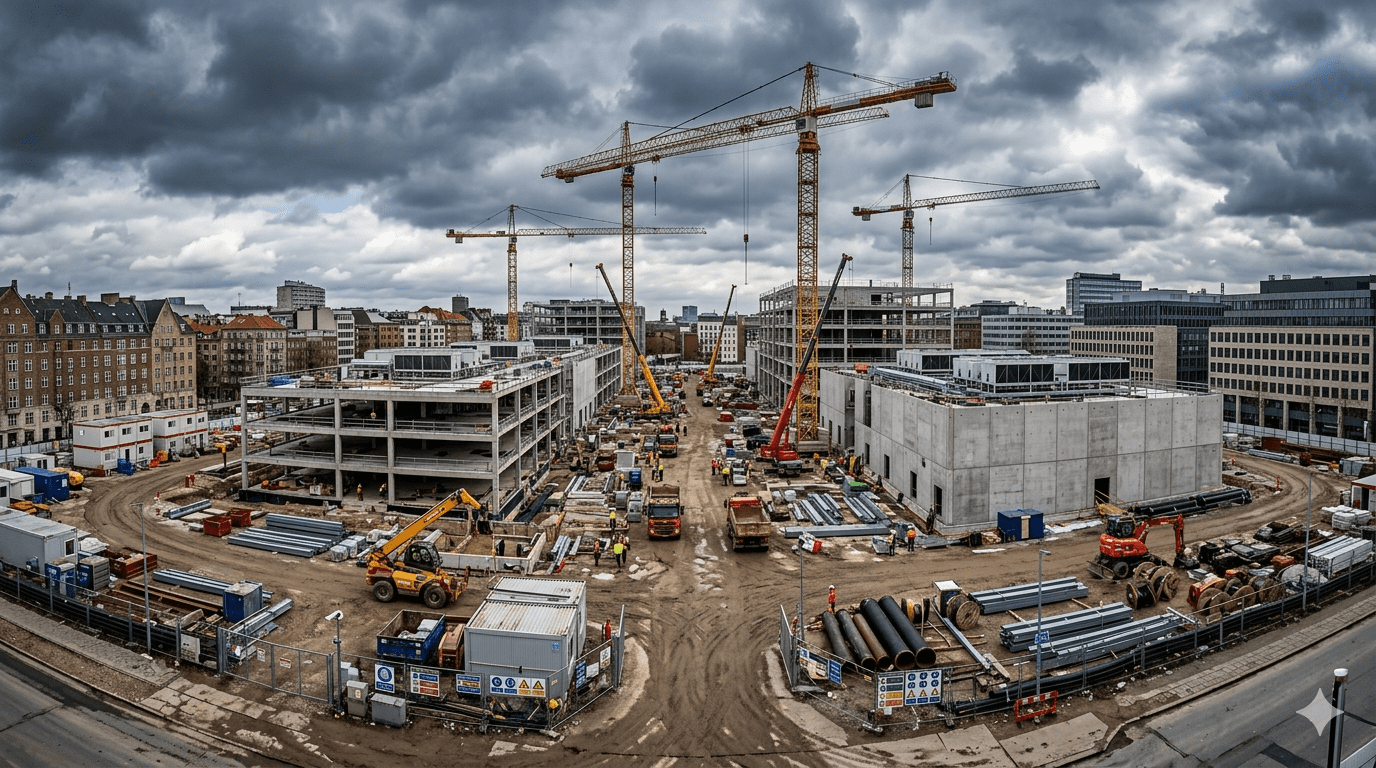

When OpenAI paused its UK Stargate project in April, the stated reasons were energy costs and regulatory uncertainty. Neither was surprising to anyone who had been paying attention to Europe’s data center market over the previous eighteen months. What was surprising was how directly OpenAI said it. The company told CNBC it would move forward on Stargate UK “when the right conditions such as regulation and the cost of energy enable long-term infrastructure investment.” That sentence is a verdict. It says that Europe, specifically the UK, currently lacks the conditions that make billion-dollar AI infrastructure investment viable. For a continent that has declared AI competitiveness a strategic priority, that verdict demands a serious response.

The Stargate UK pause is the most visible symptom of a structural problem that affects the entire European data center market. Europe’s primary data center hubs, London, Dublin, Amsterdam, Frankfurt, and Paris, are operating below 8% vacancy with significant grid interconnection delays. Demand is accelerating while supply constraints are tightening. The European Data Centre Association projects electricity demand growth of roughly 15% annually through the decade. Against that backdrop, the EU is preparing to release a Data Centre Energy Efficiency Package in Q2 2026 that will introduce a new rating scheme for data centers alongside minimum performance standards. Germany has already enacted waste heat reuse requirements for new builds. These regulations reflect genuine environmental priorities. However, they are landing at a moment when the infrastructure market has no spare capacity to absorb additional compliance complexity.

The Fragmentation Problem at the Core

The most significant regulatory challenge facing European data center development is not any single rule but the fragmentation of the regulatory environment across member states. A developer building a hyperscale facility in the US navigates federal permitting alongside state-level requirements. A developer building across multiple European markets navigates entirely different planning systems, grid connection processes, environmental assessment requirements, and energy efficiency mandates in each jurisdiction. The compliance cost and timeline uncertainty of this fragmentation is material, and it falls most heavily on the projects that Europe most needs to attract.

Germany’s waste heat requirement illustrates the problem precisely. The mandate is environmentally sensible. Requiring new data centers to capture and reuse the heat they generate rather than discharging it to the atmosphere reduces net energy consumption and aligns data center development with district heating infrastructure. However, as JLL’s European data center research team noted, the municipal heat utilization infrastructure that the waste heat requirement assumes often does not yet exist in the locations where data center development is most commercially attractive. The regulation therefore steers data center development toward locations with existing district heating networks rather than toward locations with available power and competitive land costs, creating a misalignment between where the regulation pushes development and where operators can actually build viable projects on commercial timelines.

Where Investment Is Flowing Instead

The investment that is not reaching Europe’s primary markets is not disappearing. It is redirecting to markets that offer more favorable combinations of power access, permitting speed, and regulatory clarity. Spain and Italy are absorbing a significant share of the European hyperscaler investment that would previously have gone to London, Dublin, or Amsterdam. Madrid’s hyperscaler-friendly policy environment and its role as a subsea cable landing point have made it the fastest-growing data center market in Europe by percentage growth. Milan is following a similar trajectory. Both markets offer the combination of renewable energy access, available land, and supportive regulatory environments that primary markets can no longer reliably provide.

Norway represents the most compelling European alternative for operators prioritizing renewable energy and cooling efficiency. OpenAI’s Stargate Norway project, powered entirely by hydroelectric energy and benefiting from natural cooling, is proceeding actively even as Stargate UK has been paused. The contrast is instructive. The same company paused in one European jurisdiction is building aggressively in another because the conditions that make long-term infrastructure investment viable are present in one and absent in the other. As covered in our analysis of the time-to-power crisis as AI’s hidden scaling ceiling, the regulatory and physical infrastructure constraints on AI data center development are interconnected in ways that make no single constraint resolvable in isolation. Europe’s regulatory problem cannot be separated from its energy infrastructure problem because both operate on the same project timelines and affect the same investment decisions.

What the EU’s Regulatory Package Will and Will Not Solve

The European Commission’s Data Centre Energy Efficiency Package, planned for Q2 2026 adoption alongside the Cloud and AI Development Act, addresses the sustainability dimension of Europe’s data center challenge. Its rating scheme and minimum performance standards will create a common European framework for measuring and comparing data center energy efficiency that currently does not exist. That is a genuine improvement in regulatory coherence that the market needs. However, the package does not address the permitting fragmentation that makes project approval timelines unpredictable across member states, the grid connection processes that can delay large facilities by years, or the planning system complexity that OpenAI cited as a factor in its UK withdrawal.

The Cloud and AI Development Act, which aims to triple Europe’s data center processing capacity within five to seven years through streamlined approvals and public funding for energy-efficient facilities, addresses the capacity gap more directly. However, tripling capacity in five to seven years against a baseline where primary markets are already capacity-constrained requires permitting timelines that EU member states have not historically delivered for large industrial projects. The gap between the Commission’s capacity ambitions and the member states’ planning system realities is where European AI infrastructure strategy most visibly struggles. Furthermore, as explored in our analysis of the announced versus built gap in AI infrastructure, the distance between what gets announced and what gets built is the defining risk of this infrastructure cycle. Europe’s regulatory package will produce announcements. Whether it produces capacity depends on implementation at the member state level, where the Commission has limited direct authority.

What Europe Actually Needs to Do

The honest assessment of Europe’s data center regulatory challenge requires separating what the EU can control from what member states must deliver. The Commission can create common frameworks, provide funding incentives, and issue guidance. It cannot streamline planning systems in Germany, accelerate grid connection queues in the UK, or resolve the local opposition dynamics that are slowing projects in the Netherlands and Ireland. Those require member state action, and the urgency of that action is not yet reflected in the pace at which most European governments are moving.

The UK faces a specific version of this challenge. Post-Brexit, it operates outside EU regulatory frameworks but has not created a sufficiently differentiated alternative that would make it more attractive than EU member states for large-scale AI infrastructure investment. The UK government’s withdrawal of proposed copyright flexibility for AI developers, cited by OpenAI as a relevant factor in the Stargate UK pause alongside energy and permitting concerns, adds a layer of policy uncertainty that infrastructure investors did not have to navigate in earlier years.

The combination of high energy costs, complex planning systems, and an unresolved AI policy framework is producing exactly the outcome that OpenAI’s statement described. Europe has huge potential for AI. It does not currently have the conditions that make billion-dollar infrastructure investment viable at the pace and scale the AI race demands. Closing that gap requires regulatory action that matches the urgency of the problem, not the pace of the legislative cycle.