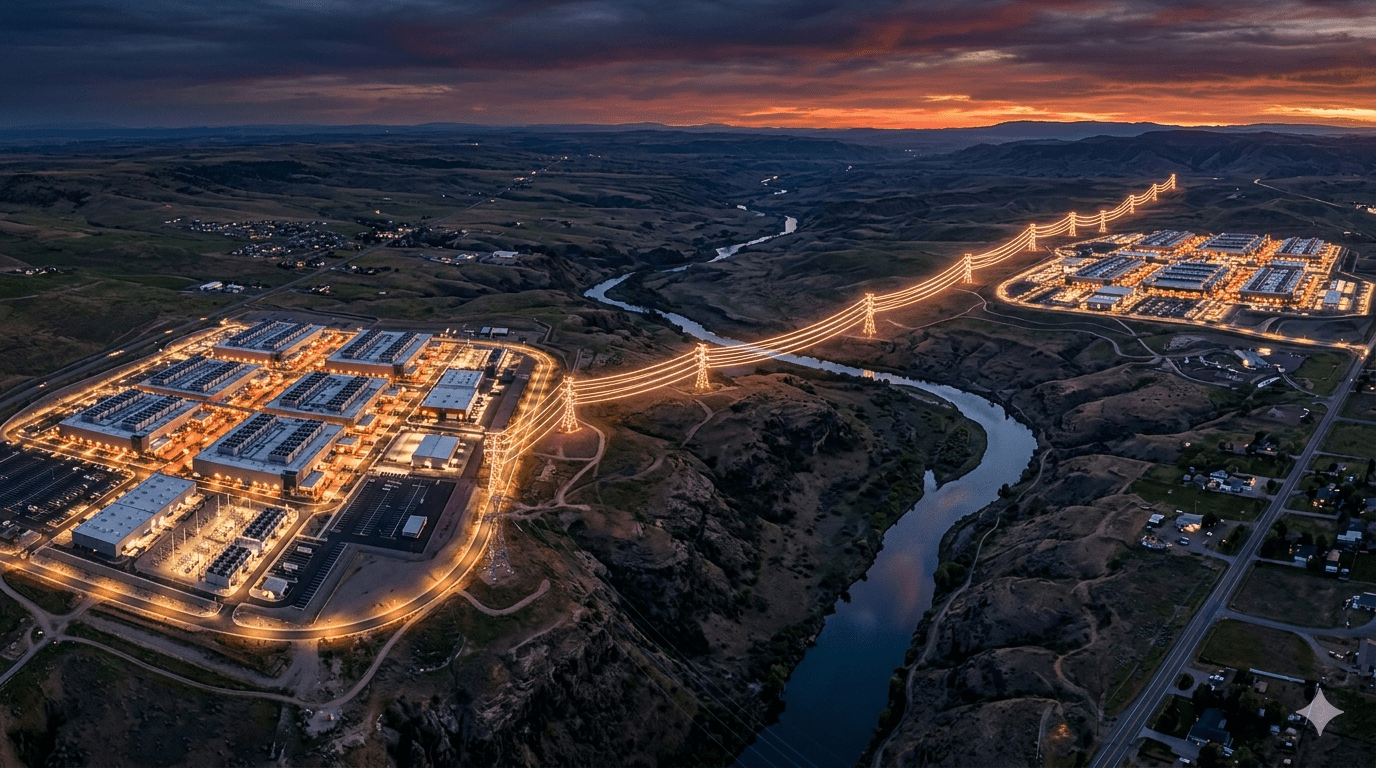

The Google-Anthropic deal that landed last week has been covered primarily as a financial story. Google investing up to $40 billion in Anthropic at a $350 billion valuation is genuinely significant capital news. However, the financial terms are not the most consequential part of the deal. The most consequential part is the 5 gigawatts of computing capacity that Google will supply to Anthropic over five years, which sits alongside a separate 5 gigawatt commitment from Amazon under its own $25 billion investment arrangement. Anthropic now has 10 gigawatts of AI compute reserved across two independent hyperscaler supply chains. That is not a financing story. That is an infrastructure story, and it is one of the most significant infrastructure stories of the year.

Consider what 10 gigawatts of compute actually means in physical terms. A single gigawatt of AI compute capacity costs between $35 billion and $50 billion to build, according to industry estimates. The full 10 gigawatt commitment therefore implies somewhere between $350 billion and $500 billion in infrastructure investment to deliver it. That is the cost of building the physical facilities, installing the power infrastructure, commissioning the cooling systems, and deploying the GPU or TPU clusters that the capacity represents. Anthropic is not building any of this itself. Google and Amazon are building it for Anthropic, against a commitment that Anthropic will consume it. That structure, a model developer pre-reserving infrastructure at gigawatt scale before it is built, is genuinely new. It is changing the logic of how hyperscaler infrastructure investment decisions get made.

Why Pre-Sold Capacity at This Scale Is Different

Infrastructure finance has always depended on demand visibility. A developer builds a facility when they have reasonable confidence that tenants or customers will consume the capacity it provides. Traditionally, that confidence came from existing customer relationships, market demand forecasts, and the general growth trajectory of cloud adoption. Hyperscalers building their own capacity made investment decisions based on internal demand projections and competitive positioning rather than committed external customers. The Google-Anthropic and Amazon-Anthropic deals represent something structurally different. They are pre-sold capacity commitments at a scale that directly drives infrastructure investment decisions before a single shovel breaks ground.

Google does not need to forecast whether there will be demand for 5 gigawatts of TPU compute. Anthropic has committed to consuming it and has committed $100 billion to doing so. That commitment converts a demand projection into a contracted obligation, and a contracted obligation is a fundamentally better basis for a multi-hundred-billion-dollar infrastructure investment than any forecast. Furthermore, the commitment extends Google’s custom silicon flywheel in a way that generic cloud capacity cannot. Anthropic’s workloads will run on Google’s TPU architecture, which means every dollar of Anthropic’s AI development generates operational data that Google uses to improve its TPU design, optimize its infrastructure, and deepen its understanding of frontier AI workload requirements. The 5 gigawatt capacity deal is therefore simultaneously a revenue commitment, an infrastructure financing signal, and a research collaboration that competitors cannot easily replicate.

What This Means for the Neocloud Sector

The implications of the pre-sold capacity model for the neocloud sector are uncomfortable and deserve honest examination. Neoclouds built their businesses on the premise that frontier AI developers would need GPU capacity that hyperscalers could not supply fast enough or at competitive cost. That premise was accurate in 2023 and 2024 when GPU scarcity and hyperscaler capacity constraints made neoclouds genuinely necessary for developers who could not wait. The Anthropic deals suggest that premise is becoming structurally less accurate as hyperscalers move to lock frontier model developers into multi-year, multi-gigawatt capacity commitments that make neocloud alternatives less relevant at the scale that matters most.

Anthropic with 10 gigawatts committed to Google and Amazon does not need CoreWeave, Lambda, or any other neocloud provider for its primary compute. It may continue to use neocloud capacity for specific workloads, overflow capacity, or redundancy purposes. However, the strategic compute relationship that drives Anthropic’s infrastructure planning and its capital allocation is now locked into two hyperscaler ecosystems for a decade. As covered in our analysis of the AI factory model replacing conventional data center infrastructure, the frontier AI labs that control their infrastructure relationships control their research velocity. The labs that have locked in hyperscaler capacity at gigawatt scale have converted infrastructure from a constraint into a competitive asset. The neoclouds that hoped those labs would remain long-term anchor customers are discovering that hyperscaler investment changes the calculus entirely.

The Physical Execution Risk Nobody Is Discussing

The financial and strategic dimensions of the Anthropic deals have received extensive coverage. The physical execution risk embedded in them has received almost none. Five gigawatts of TPU compute is not a product Google can order from a supplier and deliver on a schedule measured in months. It is a multi-year physical engineering project that requires land acquisition across multiple sites, grid interconnection in markets with queues measured in years, water rights in locations where water is increasingly constrained, cooling infrastructure at densities that have never been commercially deployed at this scale, and power purchase agreements or generation assets to supply clean energy to facilities that will draw more power than many cities.

Every one of those inputs has a timeline that is not fully within Google’s control, regardless of how much capital it commits. The $30 billion tranche of Google’s Anthropic investment is contingent on Anthropic hitting performance milestones. Those milestones depend partly on Google delivering the infrastructure capacity on the schedule the deal implies. If Google’s execution on any of the physical infrastructure inputs slips, the capacity Anthropic has committed to consuming may not be available when Anthropic needs it, with consequences for both companies’ competitive positions. As noted in our analysis of the time-to-power crisis as AI’s hidden scaling ceiling, the gap between capital commitment and operational infrastructure is one of the defining risks of the current AI buildout cycle. The Anthropic deals are the largest individual expression of that risk in the market today.

The Model That Everyone Will Try to Copy

The Google-Anthropic and Amazon-Anthropic structures will be studied and replicated by every participant in the AI infrastructure market over the next two years. Hyperscalers that have not yet locked frontier model developers into multi-gigawatt committed capacity relationships will attempt to do so. Model developers that have not yet secured hyperscaler capacity commitments will seek them, recognising that uncommitted developers face a future in which the best infrastructure is pre-allocated to competitors who moved earlier. Infrastructure developers and investors will build financial models around pre-sold capacity as a primary underwriting criterion rather than a bonus feature.

The market that emerges from this transition will look structurally different from the one that entered it. Pre-sold gigawatt-scale capacity commitments will anchor major hyperscaler infrastructure investment decisions. Model developers that secured those commitments early will hold structural compute advantages that latecomers cannot easily close, regardless of capital availability. At the same time, the infrastructure financing market will develop new instruments and frameworks tailored to the pre-sold capacity model, because existing structures assume forecast demand rather than contracted demand. That model is fading. The Anthropic deals provide the clearest signal yet of what is replacing it.