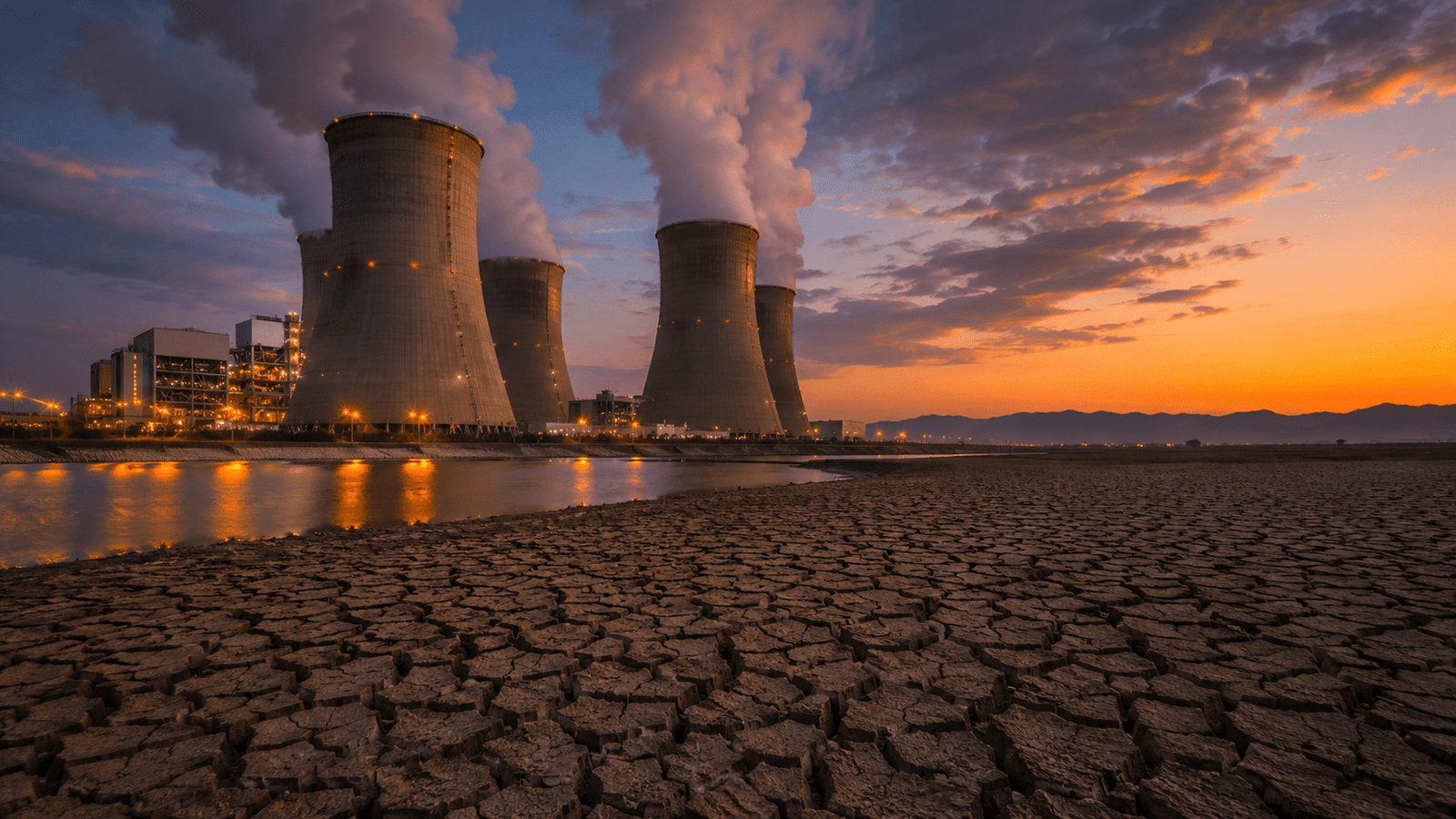

The AI infrastructure conversation has been dominated by power. Grid connection queues, transformer shortages, utility rate disputes, and behind-the-meter generation have all received extensive coverage as the binding constraints on how fast and where operators can build AI data centers. Water, by contrast, has remained a secondary constraint that stayed visible in the background without commanding the same urgency. That is now changing. Morgan Stanley projects that AI data center water consumption for cooling and electricity generation will reach approximately 1,068 billion litres annually by 2028, representing an 11-fold increase from 2024 estimates. The scale of the increase is significant on its own. However, the geography of where operators will need that water is what turns it from a large consumption figure into a structural constraint.

Nearly one-third of new data center builds face higher water scarcity risks by 2050, according to MSCI’s analysis of 13,558 data center assets worldwide. The markets where data center development is most concentrated — Northern Virginia, Phoenix, Texas, and parts of California — are among the markets where water stress is most acute. Phoenix’s Maricopa County has implemented water budgets for large industrial users. Texas aquifer depletion is affecting long-term water availability in multiple data center markets. Google reported using more than 5 billion gallons of water across all its data centers in 2023, with 31% of its freshwater withdrawals coming from watersheds already experiencing medium or high water scarcity. The operational and reputational risk of that geographic concentration is material and growing with every new gigawatt of AI capacity added to water-stressed markets.

The Three Water Scopes That Operators Are Not Fully Accounting For

The water footprint of AI infrastructure operates across three distinct scopes that most operator reporting addresses incompletely. Scope 1 is on-site data center cooling — the water that cooling towers evaporate or direct cooling systems use at the facility itself. This is the water consumption dimension that most operator sustainability reports address, though they rarely do so with enough specificity to allow meaningful comparison across facilities and markets. Scope 2 is the water consumed in electricity generation — the cooling water that power plants use to supply grid electricity to data centers. Operators frequently omit this dimension from water reporting even though, according to Morgan Stanley analysis, it typically represents the largest component of total water footprint when grids source electricity from thermal generation.

The Hidden Water Cost of Semiconductor Manufacturing

Scope 3 is semiconductor manufacturing water consumption — the ultrapure water used in chip fabrication that is embedded in the AI hardware the data center operates. Semiconductor facilities can consume up to five million gallons of ultrapure water daily, and the water intensity of GPU manufacturing at advanced process nodes is substantially higher than for conventional semiconductors due to the additional cleaning, planarisation, and rinsing steps required. The full three-scope water footprint of AI infrastructure is substantially larger than the on-site cooling water that operator sustainability reports typically disclose, and the gap between disclosed and actual water consumption is growing as AI GPU density and manufacturing complexity increase simultaneously.

The disclosure gap across all three scopes has a compounding effect on how water risk is evaluated in data center investment and development decisions. When operators report only Scope 1 cooling water, they present a water footprint that is a small fraction of their actual total consumption. Investors evaluating data center assets on the basis of disclosed water consumption are therefore systematically underestimating the water risk embedded in those assets, particularly in markets where Scope 2 electricity generation is from thermal sources with high cooling water requirements. The gap between disclosed and actual water consumption is not primarily a transparency failure — most operators are disclosing what the frameworks require them to disclose. It is a framework failure, and the frameworks are not updating fast enough to capture the water footprint of AI infrastructure at the scale it is now reaching.

The Site Selection Implication That Changes the Development Map

The water constraint is already shifting where new AI data center development remains economically and operationally viable in ways that announced development pipelines do not yet fully reflect. Markets with abundant renewable water sources — the Nordic countries, Quebec, the Pacific Northwest, and parts of New Zealand — are attracting AI infrastructure investment partly because of water availability rather than solely because of power cost and land access. OpenAI‘s Stargate Norway project, which runs on hydroelectric power in a market with abundant water, most clearly expresses a development strategy that accounts for both power and water constraints simultaneously.

The water constraint interacts with the power constraint in ways that compound site selection complexity. The renewable energy sources that are most attractive for AI infrastructure — solar in desert markets, wind in coastal markets — are often located in markets with the greatest water stress. Solar-powered data centers in Arizona and Nevada solve the carbon problem while creating a water problem that the same sustainability framework is supposed to avoid. The markets that offer both abundant renewable energy and abundant water — Norway, Iceland, parts of Canada — are precisely the markets that prior analysis of Europe’s AI infrastructure race identifies as best positioned to attract investment that constrained primary markets cannot accommodate.

Water availability is becoming a positive selection criterion for AI infrastructure location in a way that reinforces the geographic diversification trend that power constraints are already driving. Operators mapping their development pipelines against both power and water availability simultaneously are making better long-term site selection decisions than those mapping against power alone.

The Regulatory and Disclosure Gap That Needs Closing

The water disclosure and regulatory framework for data centers lags years behind the frameworks governing power disclosure and regulation, and that gap creates risks that neither operators nor investors adequately account for. Utilities report, regulate, and price power consumption through utility meters, grid interconnection agreements, and power purchase agreements that establish clear contractual and regulatory frameworks. By contrast, operators measure and report water consumption inconsistently, while a patchwork of state water law frameworks governs it through requirements and enforcement mechanisms that vary enormously.

The AGU Advances paper published in February 2026 on data center water footprints concluded that the industry needs a coordinated approach, including standardising water use reporting at the facility level, incentivising adoption of low or no-water cooling technologies, and integrating water availability assessment into data center site selection. However, neither operators nor regulators have implemented those recommendations at scale. As a result, investors evaluating data center assets cannot reliably compare water risk across facilities, communities cannot access the information they need to make informed decisions about development approvals, and operators cannot demonstrate water management performance in ways that regulators and investors can meaningfully evaluate. Closing that gap requires the same combination of voluntary operator commitment and mandatory regulatory minimum that progressively improved power consumption disclosure over the past decade.

The Cooling Technology Shift Already Underway

The technology response to water scarcity is already visible in how leading operators are redesigning their cooling infrastructure. Rear-door heat exchangers and direct-to-chip liquid cooling systems that use closed-loop circuits reduce evaporative water consumption by 90% or more compared to conventional cooling tower approaches. Meta’s Huntsville, Alabama facility uses a closed-loop system that eliminates evaporative cooling entirely. Microsoft has committed to being water positive by 2030, meaning it will replenish more water than it consumes across its global operations, a commitment that is driving rapid adoption of closed-loop cooling at new facilities and retrofitting programmes at existing ones. The operators investing in water-efficient cooling technology now are not simply meeting sustainability commitments. They are building operational infrastructure that will prove commercially essential as water constraints tighten in the markets where AI infrastructure is most concentrated.