The competition for data center investment has become one of the defining economic development contests of the 2020s. Every level of government from municipal industrial development agencies to national treasuries is offering some combination of tax exemptions, land grants, utility rate concessions, and permitting fast-tracks to attract hyperscaler and AI infrastructure investment. The offers have grown more generous with each cycle as governments observe what their neighbors are offering and conclude that matching or exceeding those terms is the price of staying in the competition. The result is a global arms race in data center incentives that is producing outcomes nobody quite intended when the first data center tax break was written.

The fundamental problem is structural. Policymakers designed data center tax incentive frameworks for manufacturing. They assumed that large capital investments would generate substantial permanent employment, and that foregone tax revenue would be recovered through employment taxes, payroll spending, and local supply chain activity. Data centers break each of those assumptions. A billion-dollar facility that creates twenty-five permanent jobs does not behave like a billion-dollar factory that creates five hundred permanent jobs, regardless of how similar the capital commitment appears on paper. Yet agencies continue to apply the same evaluation frameworks to data center deals, often with minimal scrutiny and virtually no public accountability.

The Numbers Behind the Incentive Problem

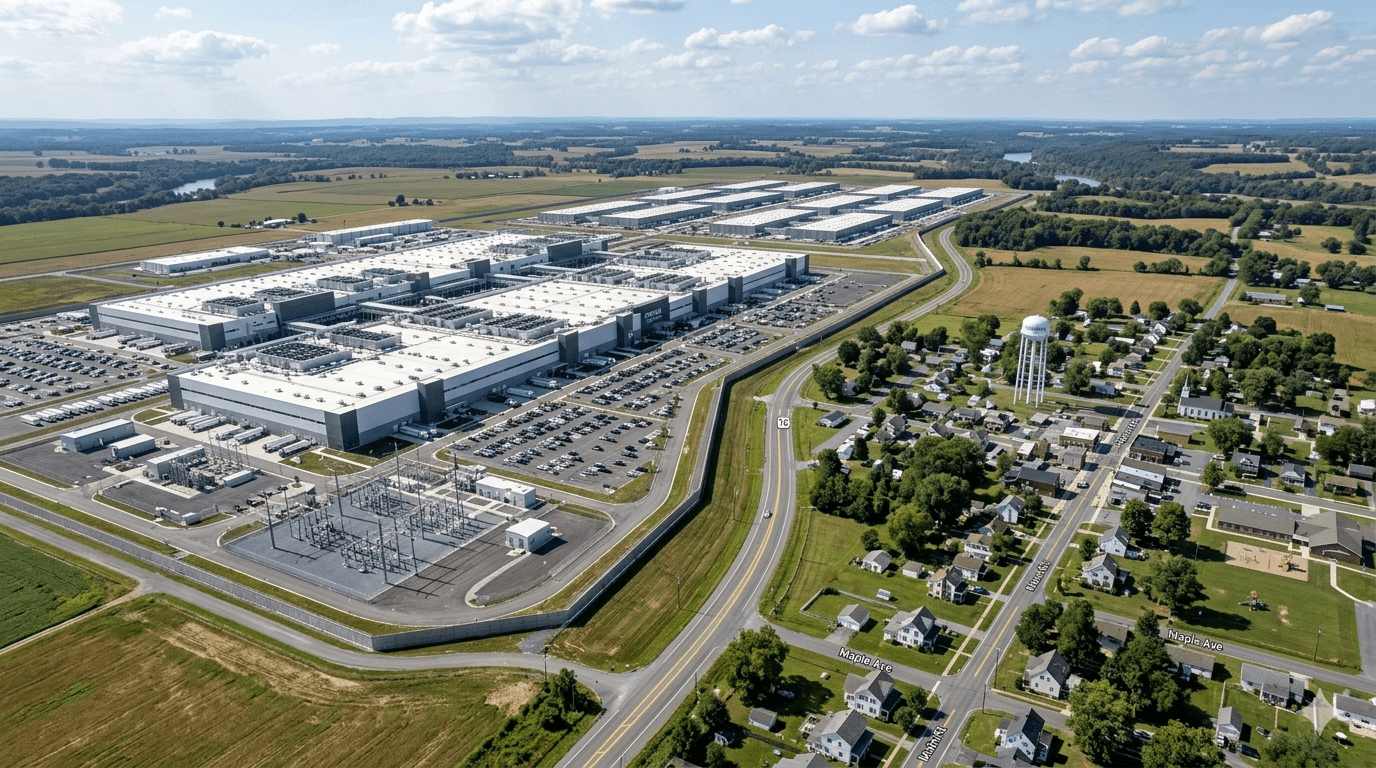

The JPMorgan Chase data center in Orangeburg, New York received nearly $77 million in tax breaks in exchange for a commitment to create exactly one permanent job. Watchdog groups describe it as the largest subsidy-to-jobs ratio for any data center deal in the country. The deal was approved by a Rockland County industrial development agency at a public hearing that nobody attended, after twenty minutes of silence and no public comment. Two weeks later it was done. The facility also had a previous round of approximately $35 million in tax breaks and at that point employed just twenty-five workers.

The Orangeburg deal is the most visible example but it is not the only one. Across the United States, data centers have received billions of dollars in tax incentives through frameworks that were never designed for this asset class. Virginia, the largest data center market in the world by installed capacity, has granted data centers sales tax exemptions on equipment purchases that amount to hundreds of millions of dollars annually. Virginia legislators have periodically attempted to reform these exemptions to require minimum employment thresholds or community benefit contributions, but the data center industry’s lobbying presence in Richmond has successfully limited the scope of those reforms in most cycles. The result is a subsidy architecture that has become entrenched through political relationships that the original policy designers never anticipated.

The Sales Tax Exemption Structure

The most common form of data center tax incentive in the United States is the sales tax exemption on equipment purchases. Data centers buy enormous quantities of servers, networking equipment, cooling systems, and power distribution units, all of which are subject to sales tax in most jurisdictions. A large hyperscale facility may spend $500 million to $1 billion on equipment alone during its initial buildout. A sales tax exemption on that purchase, at a typical rate of 6 to 8 percent, represents $30 million to $80 million in foregone public revenue. The logic behind these exemptions is that they make the jurisdiction more competitive for data center investment relative to states without exemptions, and that the aggregate economic activity of the facility justifies the revenue sacrifice. That logic requires assumptions about economic multiplier effects that the evidence does not consistently support.

A growing body of research on data center economic impact shows that the employment multiplier for data center investment is substantially lower than for manufacturing investment at comparable capital values. Manufacturing facilities generate direct employment, supply chain employment in local businesses, and induced employment from worker spending. By contrast, data centers generate limited direct employment, minimal local supply chain activity because operators procure most inputs nationally or globally, and therefore limited induced employment. As a result, the employment tax channel does not recover the tax revenue foregone through incentives in the way it often does for manufacturing. The Orangeburg deal’s economic impact analysis projected a net benefit of $100 million to the local economy, but that projection relies on temporary construction employment and tax revenue from a facility that received a 30-year property tax abatement. Closing the numbers requires generous assumptions.

The International Competition

The data center tax incentive arms race is not confined to the United States. Governments across Europe, Asia, and the Middle East are competing for hyperscaler investment with incentive packages that reflect the same structural tensions playing out in the US but in regulatory environments with different tools and different constraints.

Ireland’s data center cluster in and around Dublin developed in part because Ireland offered corporate tax rates and regulatory environments that made it attractive for US technology companies to establish European operations. The data center buildout that followed has been so extensive that Irish grid operator EirGrid has repeatedly warned that data center power demand is threatening the stability of the national grid. The Irish government is now attempting to slow data center development through planning restrictions and grid connection moratoriums, having discovered that the economic development argument for data centers looks different when the facilities are consuming a disproportionate share of a small country’s available electricity capacity.

The European Approach

European governments are navigating the data center incentive question within a regulatory framework that is substantially more prescriptive than the US approach. The EU’s state aid rules limit the kinds of subsidies that member states can offer to attract investment, requiring that incentives be proportionate, non-discriminatory, and consistent with EU competition policy. Those constraints have not eliminated European data center incentives but they have shaped their form. Rather than blanket tax exemptions, European governments tend to offer land grants, infrastructure investments, regulatory fast-tracks, and renewable energy access arrangements that are structured to comply with state aid rules while still providing meaningful economic inducements.

Spain’s designation of AI data centers as projects of national interest illustrates both the potential and the risks of the European approach. The designation gives data center developers priority access to land, including compulsory purchase powers that allow the government to acquire privately held land for data center development. AWS is reportedly sending letters to farming communities in Aragón with four-day response windows asking landowners to sell property their families have held for generations. The government’s assessment is that data center development serves a national economic interest that justifies this intervention. The farming communities affected have a different view. As we examined in our analysis of the AI industry’s community relations problem, the trust deficit between infrastructure developers and host communities is now generating political consequences that subsidy frameworks never accounted for.

The Gulf Model

The Gulf states represent a third model for data center incentive competition, one in which the incentive package is less about tax breaks and more about sovereign investment, land provision, regulatory certainty, and long-term political commitment. Saudi Arabia, the UAE, and Qatar are not primarily offering sales tax exemptions to attract data center investment. They are offering sovereign wealth fund co-investment, government-guaranteed power supply, diplomatic assurance, and the prospect of access to Middle Eastern markets and talent at scale. These are qualitatively different incentives from the US or European models and they reflect a different theory of competition for infrastructure investment.

The Gulf model has attracted substantial hyperscaler commitment. Microsoft, Google, Amazon, and Oracle all have active Gulf data center programs supported by sovereign partnerships. However, the events of March 2026, when Iranian drone strikes hit AWS facilities in the UAE and Bahrain, demonstrated that the Gulf model’s physical security assumptions had not been stress-tested at the level the current geopolitical environment requires. The sovereign guarantees that anchor the Gulf incentive model do not extend to protecting commercial infrastructure from kinetic attack in a regional conflict. That gap is now a material consideration in how investors and operators evaluate Gulf data center commitments, regardless of what the sovereign incentive package contains.

What Genuine Competition Produces

The arms race dynamic in data center incentives produces outcomes that game theory would predict, even if policymakers did not anticipate them. When multiple jurisdictions compete for the same investment by offering increasingly generous incentives, the jurisdiction that gives away the most tends to win. Investors capture the maximum available subsidy. Losing jurisdictions expend political capital developing incentive proposals that yield no return. Even the winning jurisdiction often finds that the economic returns fall short of the projections used to justify the incentive, because officials developed those projections under pressure to secure the deal rather than to assess it rigorously.

Virginia’s experience is instructive. The state has the world’s largest concentration of data center capacity, built in significant part through sales tax exemptions and other incentives. The data centers have generated substantial employment in construction trades and limited permanent employment. They have generated significant property tax revenue in Loudoun and Prince William counties, which has funded local government services and schools. They have also generated grid capacity constraints that are limiting new development, water supply pressures, community opposition that has produced political conflict, and a growing debate about whether the terms of the original incentive deals adequately reflected the full costs the facilities impose. As covered in our analysis of the time-to-power crisis as AI’s hidden scaling ceiling, the grid constraints that have accumulated in primary data center markets are in part a consequence of years of incentive-driven development that prioritised speed of capacity addition over sustainable grid planning.

The Disclosure Problem

A fundamental challenge in evaluating whether data center tax incentives produce net benefits for host communities is the lack of consistent, comparable disclosure requirements. Local industrial development agencies approve most US data center incentive deals and often operate with minimal transparency requirements. Many jurisdictions require public hearings, but agencies typically schedule them with little notice and they attract limited attention. Agencies also often withhold full details of approved deals, and follow-up reporting on whether developers meet economic development commitments is inconsistent or absent.

The result is a policy environment in which governments are making multi-hundred-million-dollar commitments of public resources with inadequate information, inadequate scrutiny, and inadequate accountability for outcomes. Food and Water Watch, which has been tracking data center incentive deals and their outcomes, has documented numerous cases where facilities that received substantial public subsidies failed to deliver the employment or economic impact that justified the original incentive offer. Without systematic disclosure and outcome reporting, there is no mechanism through which governments can learn from these failures or hold developers accountable for commitments that were central to the public justification for the deal.

What Better Policy Would Look Like

The data center tax incentive arms race does not need to be eliminated. Data centers provide real economic value, generate real tax revenue over their operating lives, and create real employment in construction, operations, and supply chain activities. The problem is not that governments are offering incentives. The problem is that the incentive frameworks are poorly designed for this asset class, inadequately transparent, and insufficiently accountable.

Better data center incentive policy would start with asset-class-specific evaluation criteria. The cost-per-job metric that dominates manufacturing incentive evaluation is not appropriate for data centers. A better framework would evaluate data center proposals on lifetime tax revenue net of incentives, grid infrastructure cost allocation, water consumption relative to local supply, community benefit commitments, and construction employment at realistic rather than optimistic levels. Several states are moving in this direction. Virginia has amended legislation to shift certain grid upgrade costs to data centers rather than socialising them across ratepayers. New York State is advancing disclosure requirements that would make data center incentive terms publicly available in a standardised format. These are incremental improvements that fall well short of structural reform but represent movement in the right direction.

The Accountability Gap

The single most impactful policy reform available to most jurisdictions would be mandatory outcome reporting on existing incentive deals. Requiring facilities that received public subsidies to report annually on employment, tax payments, grid consumption, water usage, and community benefit fulfilment would create the information base that current policy lacks. It would allow governments to evaluate whether deals that seemed reasonable at approval are delivering the outcomes that justified them. It would create accountability for developers who made commitments they did not intend to honour. And it would generate the comparative data that policymakers need to design better deals in the future.

As explored in our analysis of the announced versus built gap in AI infrastructure, the distance between what the AI infrastructure industry announces and what it delivers is a pattern that extends from project timelines to economic development commitments. Outcome reporting would not close that gap by itself, but it would make the gap visible in ways that current policy does not.

Who Is Actually Winning

The honest answer to the question of who is winning the data center tax incentive arms race is the hyperscalers and large AI infrastructure developers. They are the entities that capture the maximum available subsidy from whichever jurisdiction offers the most favourable terms. The jurisdictions that win specific deals do not necessarily win the competition in any meaningful economic sense. They win the right to host a facility that will consume their grid capacity, draw on their water supplies, generate limited permanent employment, and pay reduced taxes for years or decades under the terms of the deal they competed so hard to offer.

The communities that lose out entirely are those that see the data center built in a neighbouring jurisdiction and observe that they avoided the disruption without capturing the investment. There is a growing argument, most visible in states where community opposition has been strongest, that not hosting a data center is not obviously worse than hosting one under the typical terms of the current incentive competition. That argument has not yet entered the mainstream among economic development practitioners, but it is gaining traction in policy circles that are beginning to question whether the arms race delivers the outcomes it was meant to generate. The evidence across multiple cycles shows that it does produce data centers. Whether it produces broader development is a more complicated question that current policy frameworks do not adequately answer.

The Emerging Regulatory Backlash

The political environment around data center incentives is shifting faster than the policy environment. Community opposition that was once dismissed as NIMBYism has matured into organised legislative advocacy that is producing results at the state level. Maine passed legislation establishing what may become the first statewide moratorium on new data center construction, driven in significant part by concerns about electricity rate increases and the inadequacy of public consultation processes that approved facilities with minimal community input. New York State legislators have introduced bills that would impose moratoriums on new data centers pending comprehensive environmental impact assessments. Multiple other states are considering legislation that would reform incentive frameworks, require community benefit agreements, or impose new environmental disclosure requirements on data center developers.

The backlash is bipartisan in a way that makes it politically durable. Environmental advocates oppose data centers on water and carbon grounds. Fiscal conservatives oppose subsidies that produce minimal employment. Rural communities oppose facilities that strain local infrastructure while producing few local benefits. Agricultural communities in states like Pennsylvania and Virginia oppose rezoning that converts farmland to industrial use. This coalition does not share a unified political agenda but it shares a common interest in reforming data center incentive and permitting frameworks that were designed without their input. The industry has responded primarily through lobbying and public relations campaigns that emphasise economic benefits. That response has been effective in slowing legislative reform but has not reduced the underlying political pressure that is producing the reform impulse.

The Virginia Inflection Point

Virginia’s experience represents the most instructive case study in how the data center incentive arms race eventually produces political backlash. The state built the world’s largest data center market through years of aggressive incentive competition that prioritised capacity addition above other considerations. The result is an extraordinary concentration of digital infrastructure that generates substantial property tax revenue, employs a limited number of permanent workers, and has created grid, water, and community impacts that are now subjects of active legislative debate.

Virginia Governor Glenn Youngkin’s administration has taken a more sceptical view of data center expansion than previous administrations, reflecting pressure from rural communities in the western and southern parts of the state where data center projects have faced organised opposition. The state legislature has advanced legislation requiring data centers to bear a larger share of grid upgrade costs rather than having those costs socialised across ratepayers. Several localities have imposed or proposed moratoria on new data center development pending updated zoning and impact assessment frameworks. None of these actions reverse the existing concentration of data center capacity in Northern Virginia, but they signal a political shift that will affect the terms on which future development proceeds.

As covered in our analysis of the AI data center demand response opportunity, the relationship between data centers and the grids they depend on is under fundamental renegotiation, and the political dimension of that renegotiation is now as important as the technical dimension.

The Community Benefit Agreement Model

The most constructive alternative to the current incentive arms race that has emerged from the policy debate is the community benefit agreement model. A community benefit agreement is a legally binding contract between a developer and a community organisation that specifies the community benefits the developer will provide in exchange for community support for the project. In the data center context, community benefits might include local hiring commitments for construction and operations positions, contributions to local infrastructure improvements, energy bill assistance for low-income households near the facility, water mitigation commitments, and funding for local schools or community services.

The community benefit agreement model does not replace the tax incentive framework. It supplements it by adding a community accountability layer that standard incentive deals lack. A developer that receives $50 million in tax incentives and signs a community benefit agreement committing to $5 million in local community investment is still capturing a substantial net subsidy, but the community is capturing a defined benefit that it negotiated rather than accepting whatever the developer chose to offer voluntarily.

Meta’s Tulsa groundbreaking this year illustrates what genuine community benefit commitment looks like in practice. The company committed $25 million in local infrastructure improvements, partnered with local colleges on workforce development, and committed to covering the full cost of the facility’s water and wastewater services so those costs would not transfer to local consumers. These commitments were not legally required. They were strategically chosen to demonstrate a different model of community engagement than the industry standard.

Why More Operators Are Not Following the Meta Model

The obvious question is why more data center developers are not voluntarily adopting the community benefit commitment approach that Meta demonstrated in Tulsa. The answer is competitive pressure. A developer that voluntarily commits $25 million in community benefits is spending $25 million that a competitor who makes no such commitment does not spend. In a market where site selection decisions are made primarily on cost and incentive terms, voluntary community benefit spending is a competitive disadvantage unless it is either mandated for all developers or rewarded through the incentive framework itself.

Several localities are beginning to structure their incentive frameworks to reward community benefit commitments. A jurisdiction that offers a larger tax incentive to developers who sign community benefit agreements effectively makes the community benefit a condition of accessing the full incentive value, without mandating it as a regulatory requirement. This approach aligns the financial incentives of developers with the community interests of host jurisdictions in ways that voluntary programs cannot achieve. It is also more politically sustainable than pure regulatory mandates, because it preserves developer flexibility while ensuring that the public investment in incentives generates measurable community returns. The arms race in data center incentives will not end through voluntary industry action. It will end through the gradual accumulation of policy reforms, community accountability requirements, and disclosure mandates that make the terms of the competition more transparent and the outcomes more defensible.

What Happens Next

The data center tax incentive arms race is entering a new phase. From roughly 2015 to 2023, jurisdictions expanded incentives as they competed for an industry they did not fully understand. Since around 2024, and accelerating in 2026, scrutiny has increased as the outcomes of that first phase become visible and the limitations of the original frameworks become impossible to ignore.

The third phase, which is beginning to take shape in legislative proposals, community organising campaigns, and policy research across multiple jurisdictions, will involve structural reform of the incentive frameworks themselves. That reform will not be uniform or rapid. Different jurisdictions will reform at different speeds and in different directions, reflecting their specific political environments and the particular experiences they have had with data center development. Some will impose strict requirements. Others will maintain generous incentive programs and compete aggressively for the investment that reformed jurisdictions turn away. The diversity of approaches will itself become a competitive factor as data center developers evaluate the total cost and complexity of operating in different regulatory environments.

As explored in our analysis of how AI is changing the economics of data center site selection, the site selection calculus for AI infrastructure is already incorporating regulatory risk as a material factor alongside power, water, and connectivity. The arms race for incentives will not disappear, but jurisdictions and communities are renegotiating its terms deal by deal.