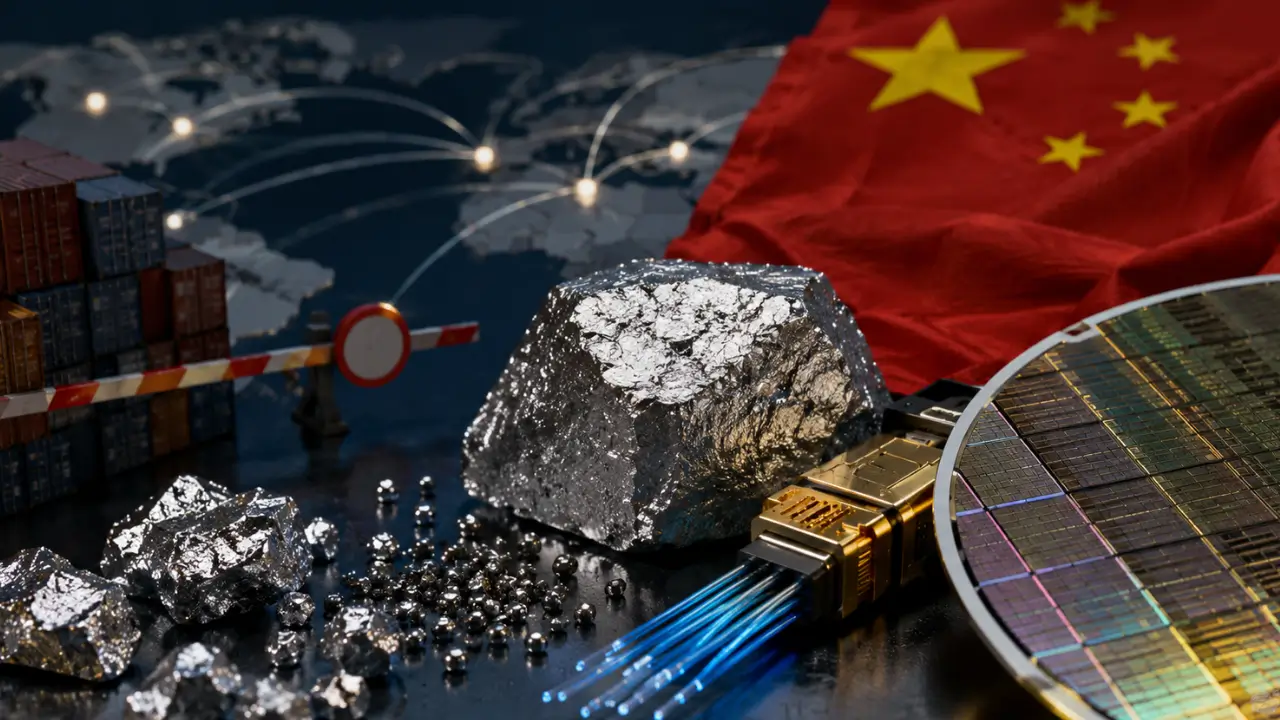

China is tightening export inspections on indium, a strategically important metal that powers advanced optical technologies used across artificial intelligence infrastructure. The move is creating fresh uncertainty for global semiconductor manufacturers and data center supply chains.

Although Beijing has not formally placed indium under export controls, recent actions by customs authorities indicate that regulators are increasing oversight of outbound shipments. Industry participants say exporters and buyers now face additional documentation requirements, including requests for detailed end-user information and longer approval timelines.

The development is attracting attention across the AI infrastructure sector because indium serves as a critical input for indium phosphide (InP), a material manufacturers use to produce high-performance optical chips. These components form the backbone of optical interconnect networks that transfer data between AI servers at increasingly higher speeds inside modern data centers. For cloud operators, semiconductor manufacturers, and networking vendors, any disruption in optical material supplies could create new bottlenecks as AI infrastructure investment continues to accelerate worldwide.

Why Indium Matters to AI Data Centers

Indium has long played a role in display manufacturing and specialized soldering applications. However, AI infrastructure has elevated its strategic importance because optical communications technologies now support many of the industry’s fastest-growing workloads. The metal serves as a precursor to indium phosphide, a material manufacturers use in advanced photonic devices and optical chips. These technologies enable high-speed data transmission across AI clusters and help operators manage the massive bandwidth demands that large language models and AI training systems create.

As AI deployments scale, optical networking has emerged as one of the most critical layers of data center architecture. Consequently, photonic manufacturing materials are gaining geopolitical significance alongside semiconductors and advanced computing hardware. China currently accounts for roughly 70% of global indium supply, giving the country a dominant position in a market that remains more concentrated than many other industrial metals markets.

Buyers Report More Intensive Export Reviews

According to market participants cited by Reuters, Chinese customs officials have recently begun seeking additional information from overseas buyers despite the absence of formal export restrictions on indium metal itself. A European raw materials buyer reported receiving a request this year from Chinese customs authorities to disclose where the final consumption destination of the indium would be. I

Industry observers view the request as a notable shift in scrutiny levels for a material that has historically moved through international markets with fewer regulatory hurdles. A large North American buyer also reported that export approval timelines have lengthened. Shipments that previously received clearance on the same day are now taking several days, a change the buyer attributed to more intensive document reviews by customs authorities. No confirmed cases of blocked indium shipments have emerged so far. Nevertheless, the additional scrutiny is creating uncertainty for procurement teams that rely on predictable delivery schedules.

The latest developments fit into a broader trend that has reshaped global technology supply chains over the past several years. China has already imposed export controls on several strategically important materials, including gallium, germanium, and graphite, all of which hold significance for advanced technology manufacturing. The increasing attention on indium has raised concerns that another critical material could become subject to tighter regulatory oversight.

Industry analysts also point to China’s decision in February last year to place indium phosphide on its export control list. Because indium phosphide is a downstream processed material derived from indium, some market participants interpret the latest customs actions as a potential extension of regulatory attention further upstream in the supply chain. Although no formal policy change has been announced, companies dependent on optical networking technologies are monitoring developments closely.

United States Moves to Build Strategic Reserves

Washington is also taking steps to reduce exposure to potential supply disruptions. The Defense Logistics Agency has announced plans to strategically stockpile up to 403 metric tons of indium over the next three years. The initiative forms part of broader efforts to strengthen supply chain resilience for critical materials linked to national security and advanced technology sectors.

The move highlights how governments are increasingly treating specialty metals as strategic assets rather than ordinary industrial commodities. As competition intensifies around AI infrastructure, securing reliable access to critical raw materials is becoming a central policy objective. Furthermore, strategic stockpiling efforts suggest that policymakers expect supply chain risks tied to critical minerals to remain a long-term concern rather than a temporary market disruption.

The changing supply landscape could create opportunities for alternative suppliers and recycling ecosystems outside China. In South Korea, Korea Zinc maintains capabilities to recover indium from zinc-processing byproducts. Japan has also developed technologies capable of extracting high-purity indium from discarded display panels, creating a potential secondary source of supply.

Elsewhere, production capacity is either operational or under development in countries including Canada, Peru, and Bolivia. For AI infrastructure investors, the emerging story extends beyond a single metal. It underscores how the next phase of AI competition may be shaped as much by access to specialized materials and industrial processing capacity as by advances in computing hardware itself.

The Compute Forecast View

The significance of China’s heightened indium inspections lies not in current shipment disruptions but in what they reveal about the evolving AI supply chain landscape. Optical networking components have become indispensable to hyperscale AI deployments, making upstream materials such as indium increasingly strategic.

If customs reviews continue to intensify, infrastructure builders may face higher procurement costs, longer sourcing timelines, and greater pressure to diversify supply channels. The AI race is often framed around chips and compute capacity, yet the availability of niche materials may prove equally influential in determining which regions can scale next-generation data center infrastructure most effectively.